Beef Wrap August 23

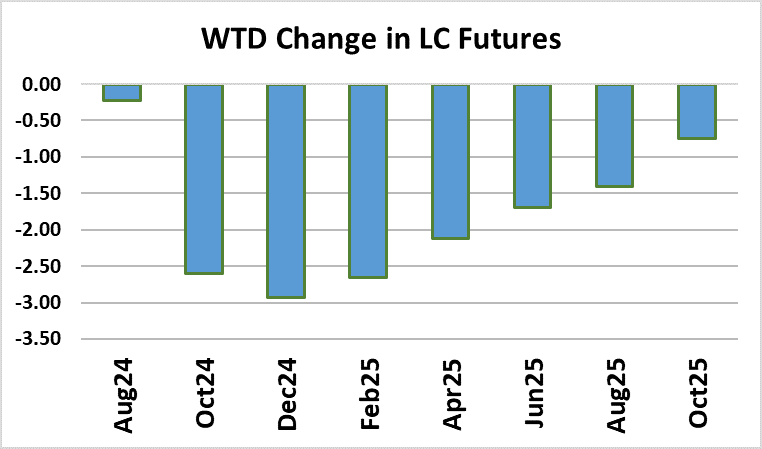

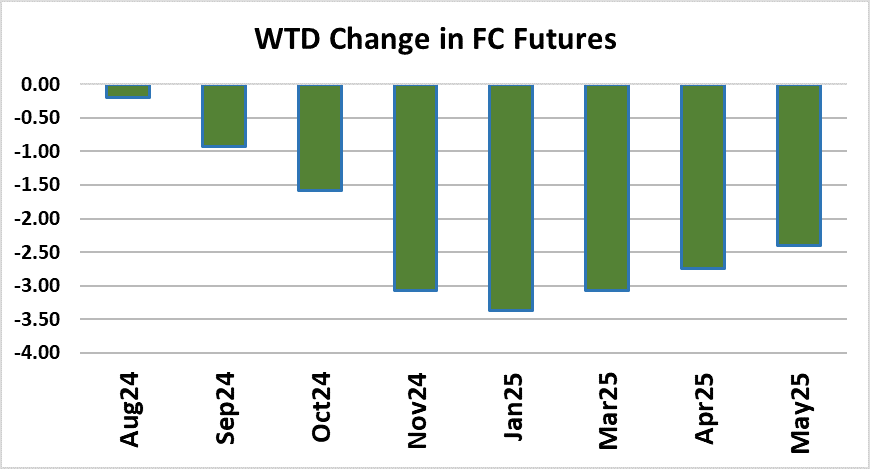

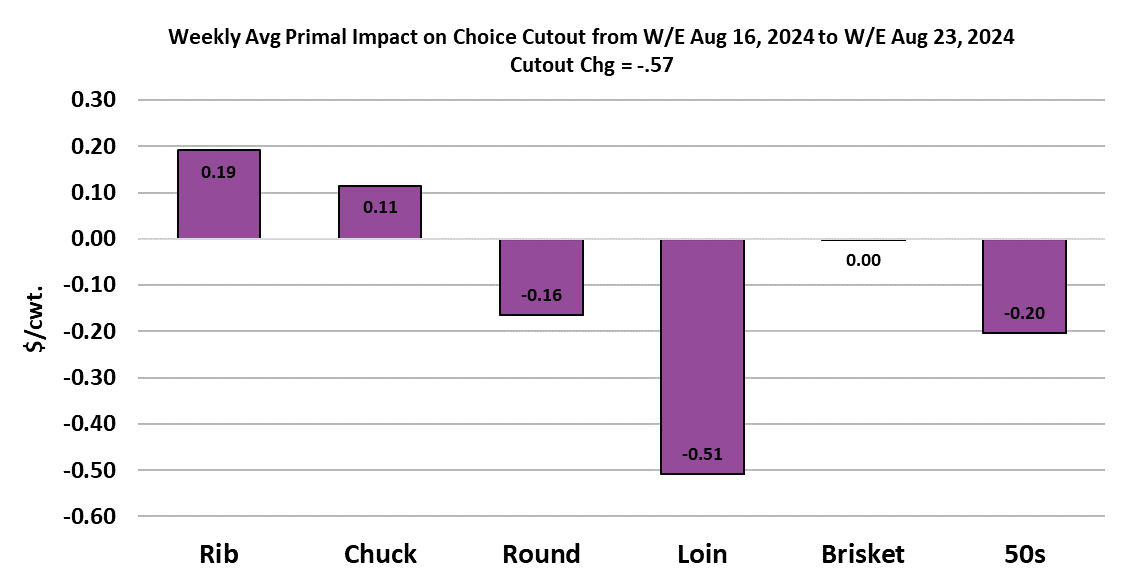

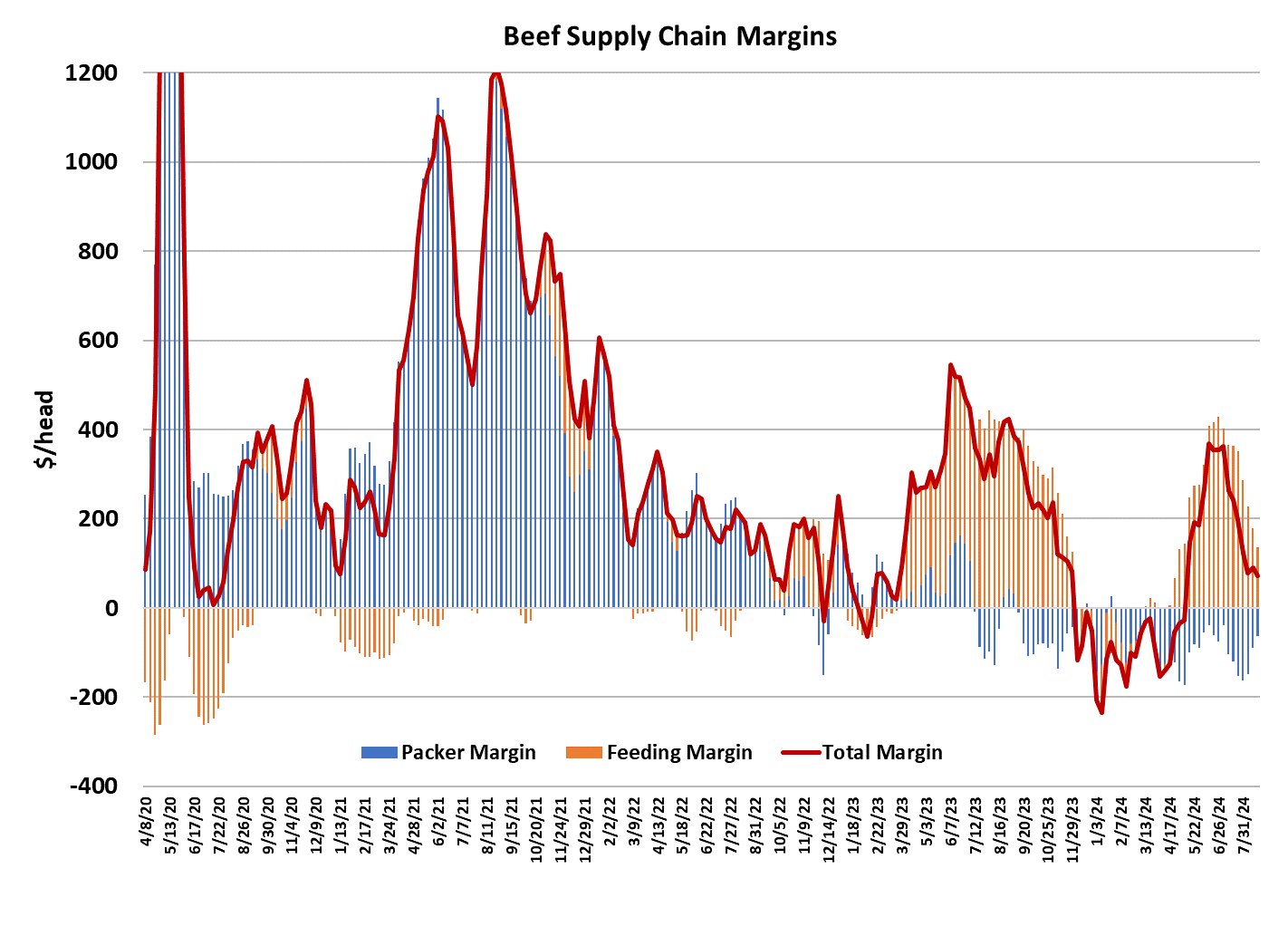

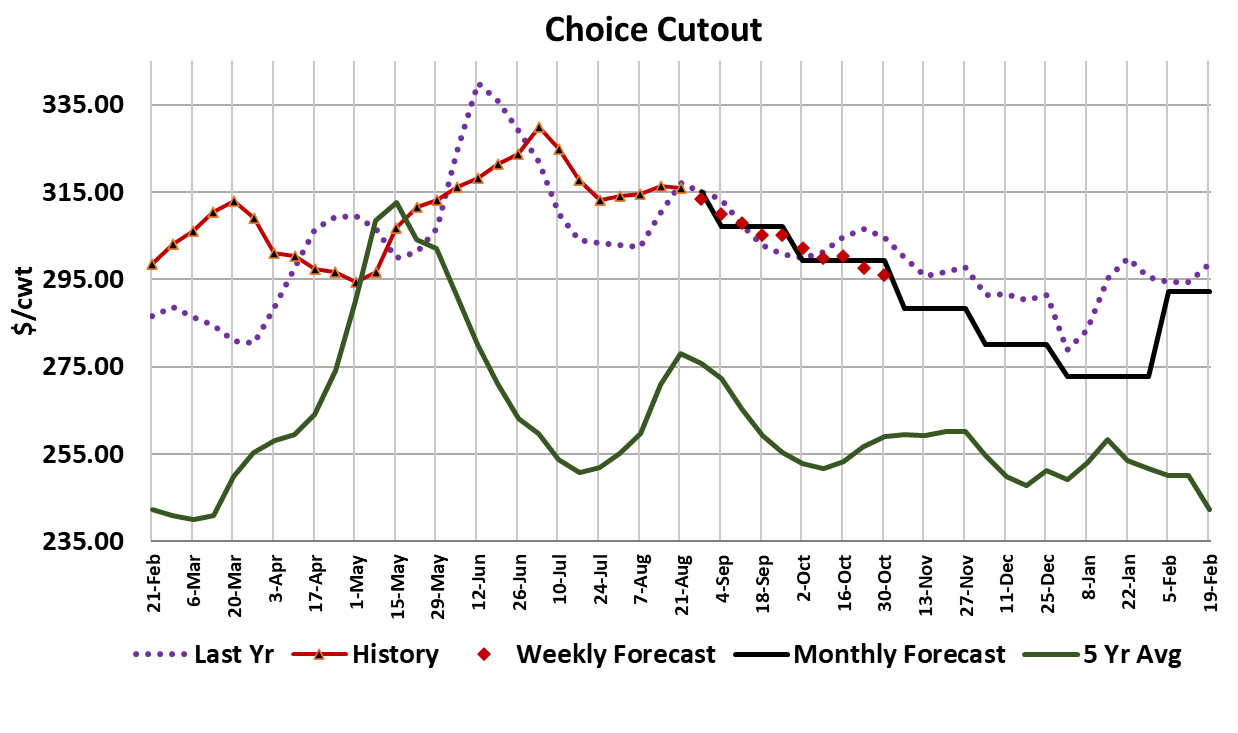

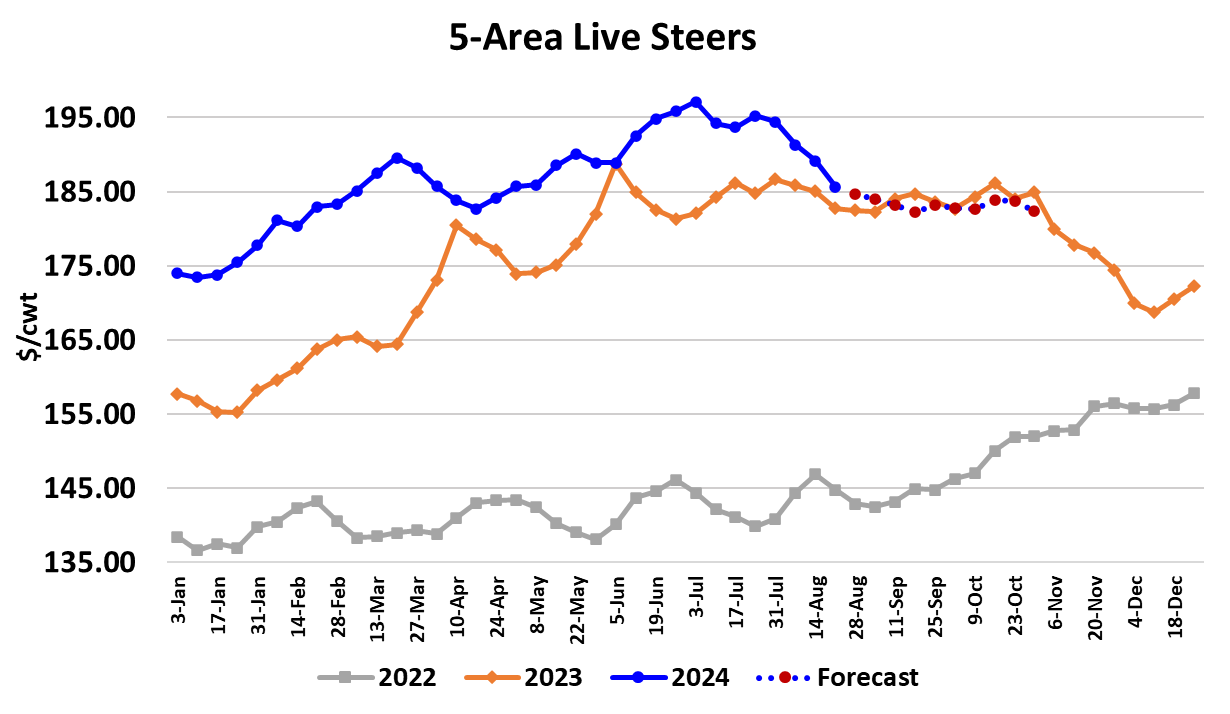

A wave of technical selling washed over live cattle futures on Tuesday and that was just more than cattle feeders could bear. Cash trade was triggered $2 lower at $183 in the South, while $184-187 was common in the North. When the all of the prices are compiled on Monday, I expect the 5-area price to print a little over $185.50. Negotiated volumes looked rather light as of Friday afternoon, so it will be interesting to see how the totals stack up on Monday. The futures sell-off early in the week allowed the most-active Oct contract to bounce off of its long-run trendline support, so perhaps that signals that traders are done punishing the LC futures for now. Today’s COF report showed July placements up 5.8% YOY, which was about 1.8% larger than what analysts were expecting. Still, the difference wasn’t huge and the Aug 1 on-feed total is still very close to last year, so perhaps this report won’t generate any further pressure in the futures next week. While the futures and the cash cattle market were melting down, prices in the beef market held up fairly well. The Choice cutout lost $0.57/cwt. on the week and the Select cutout posted a modest $0.14/cwt. gain. The loin primal was the biggest drag on the cutout while the ribs provided some modest support. All of the last-minute Labor Day buying should be complete now, but I don’t think that means the cutouts will give a lot of ground. The loins likely continue to ease, but the ribs and the end cuts appear to be on solid footing. The 90s market held firm this week near $375, so that is likely to keep interest in the end cuts relatively strong for the time being. 50s prices did start to slip near the end of the week, with the print on Friday coming in close to $145, which was a long way from the $182 print on Monday. Outside of the 50s however, the cutouts appear to be in good shape. The fundamental forecast has the Choice cutout easing slowly from here, but it isn’t likely to come down in big chunks and there is a reasonable chance that the cutouts may have a little more upside before the softening starts. The macroeconomic picture still looks relatively favorable to beef demand. The stock market quickly recovered all of what it lost a couple of weeks ago and the Fed appears poised to begin lowering interest rates in September, which could give a further boost to equity markets and the economy in general. Worries about an impending recession are still being voiced, but so far the evidence isn’t there. This week’s fed kill clocked in at 494k, up 5k from the week before and not too far below what the flow model suggests should be market ready. Packer margins have improved greatly over the past few weeks as cash cattle prices have retreated while beef prices have held firm. I calculate this week’s packer margin at -$60/head and next week that could turn into a modest positive margin as the cheaper cattle they bought this week show up for slaughter. Cattle feeders are probably growing weary of their margin shrinking and they may do their best to turn cash cattle prices higher next week, or at least keep them from going down any further. The combined margin ticked a little lower this week and may still have further downside before it makes a bottom. FI steer carcass weights were reported up 2 pounds to 925 this week and are now 24 pounds heavier than last year. Steer and heifer slaughter is running about even with last year, but the increase in carcass weights is keeping fed beef production above year ago. However, that is counterbalanced by a sharp drop in non-fed beef production as cow and bull slaughter has been down 16-18% recently. Taken together, it looks like total US beef production this week was 0.3% below last year and the blended cutout was 0.5% above the same week last year, so it is reasonable to assume that demand is maybe just a tad bit stronger than it was last year at this time. The weekly FAS data suggests that beef exports are continuing to run near the levels we saw last summer. As beef prices come down in September, we could see an uptick in export interest. For now however, the export trade appears to be lukewarm—it isn’t really hurting or helping domestic availability very much. We don’t get import data by the week, but the monthlies have shown double-digit YOY percentage increases for the past 12 months, with the most recent data (for June) showing a 15.2% YOY increase. It is pretty safe to assume that with 90s prices near $375, imports of manufacturing beef will remain strong. Next week, look for cattle feeders to be tougher negotiators and that may result in a steady or higher cash cattle market. The futures are so oversold that they will likely cheer any improvement in cash market tone, so a weekly gain could be on tap there.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}