Beef Wrap August 16

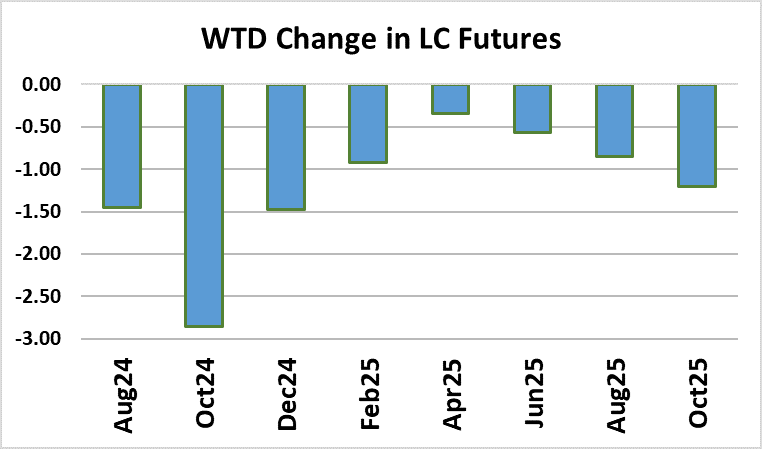

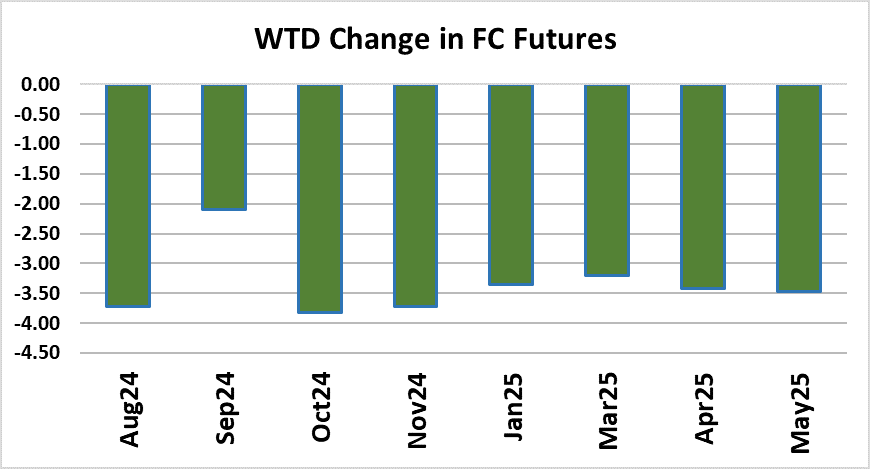

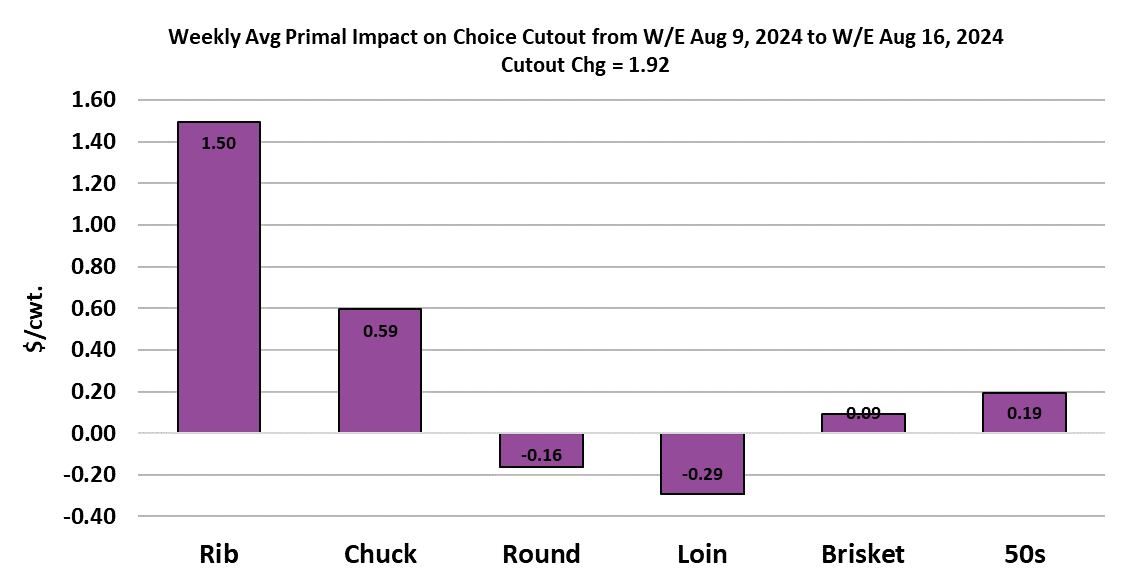

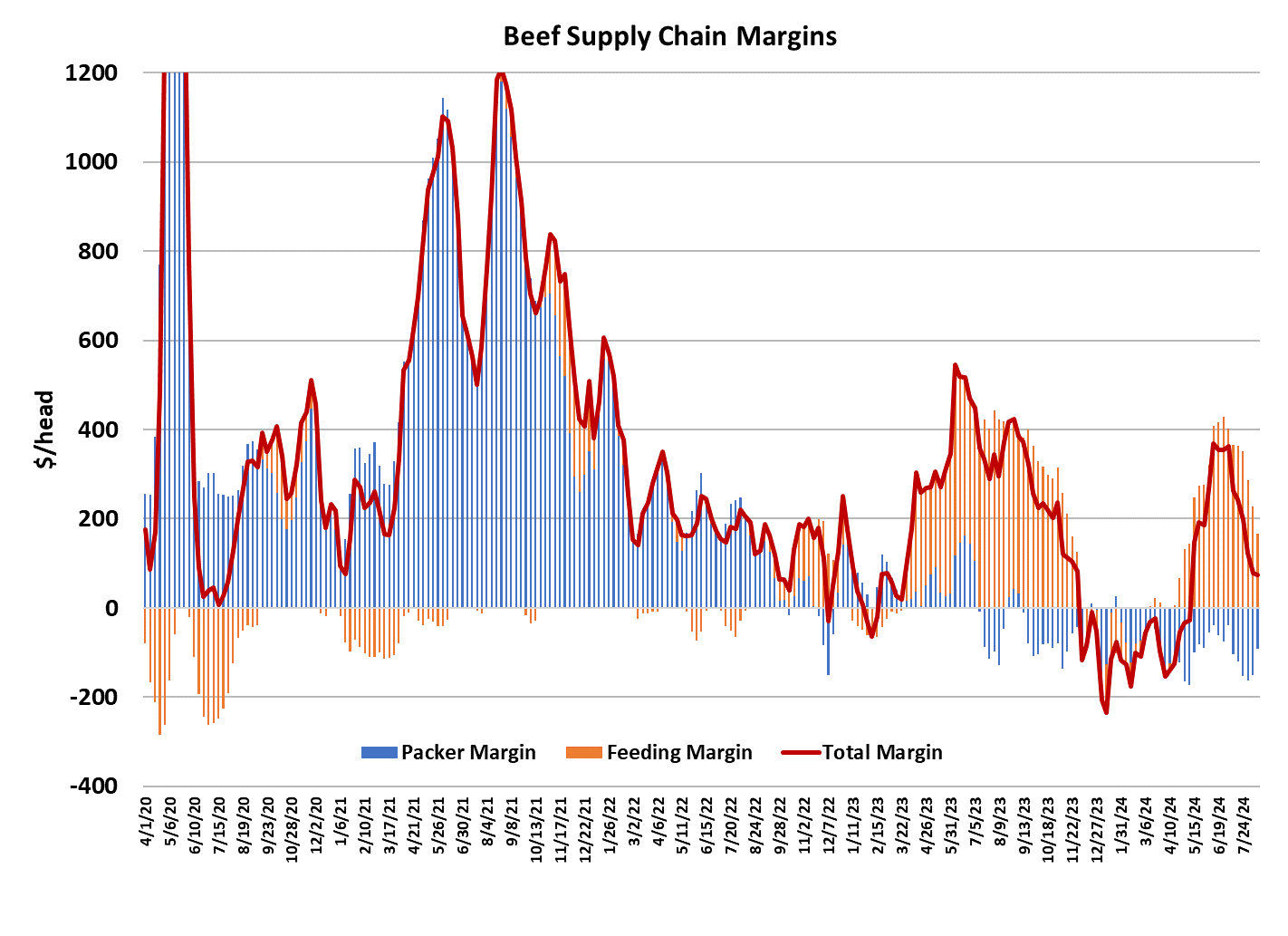

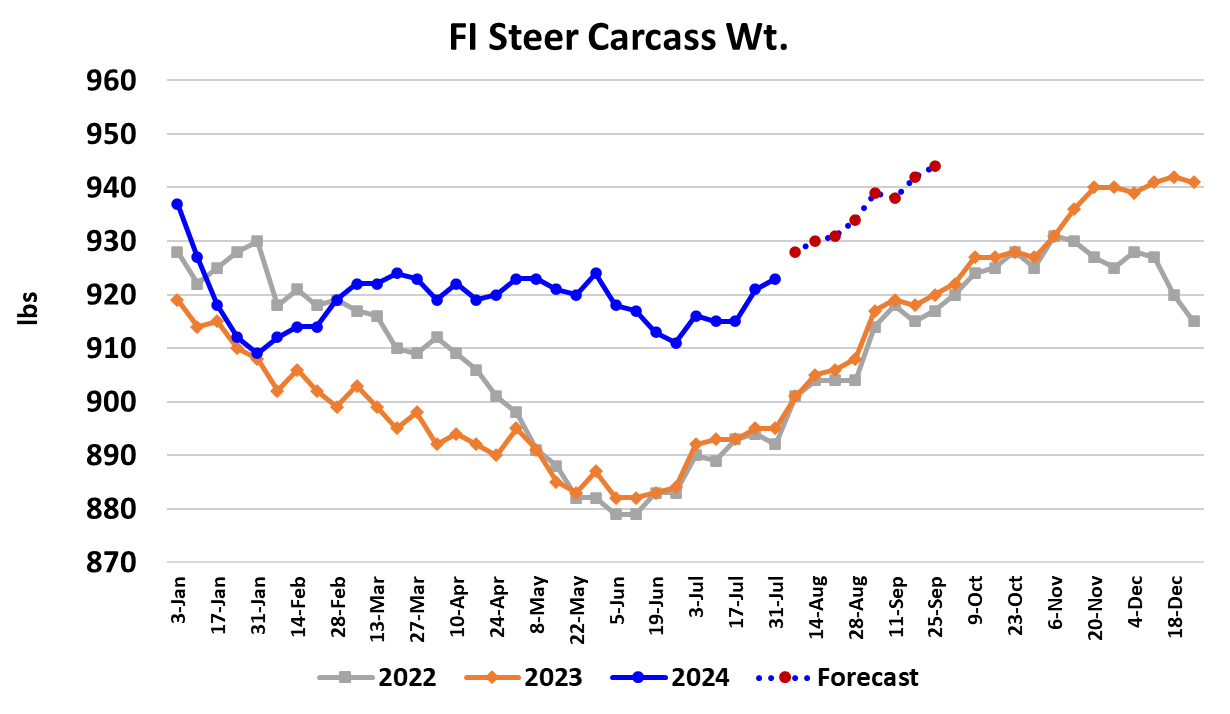

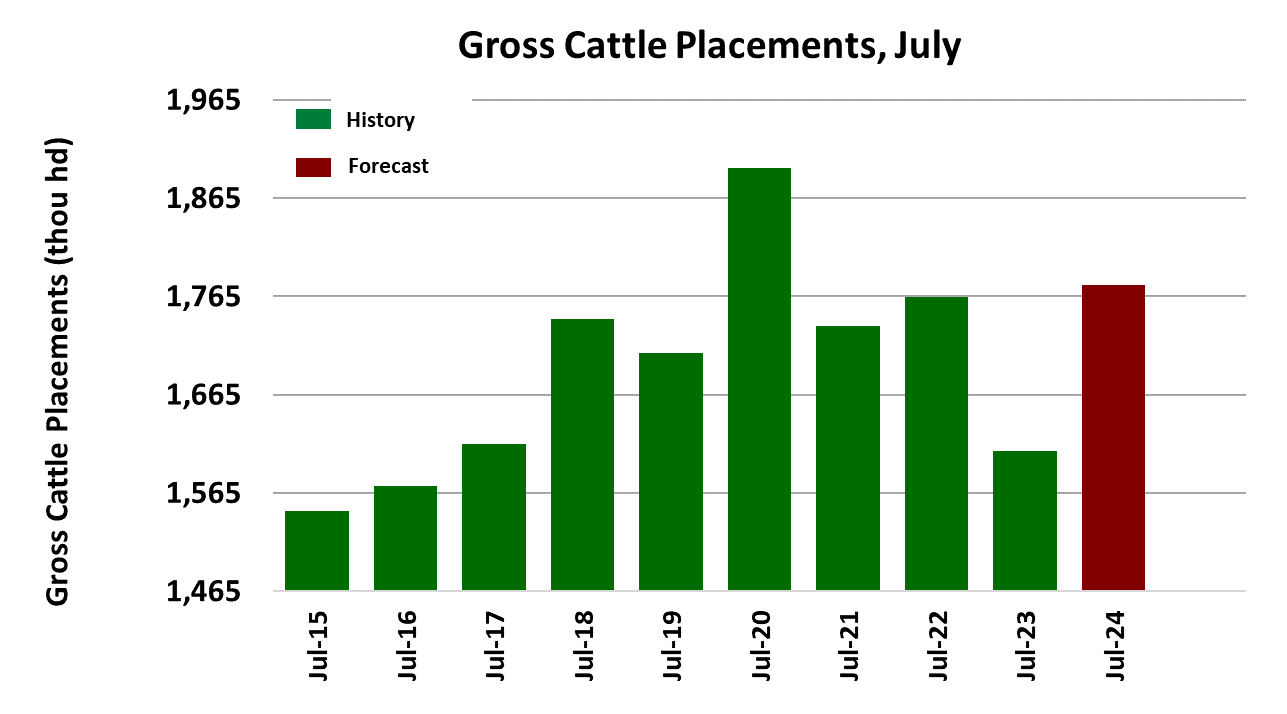

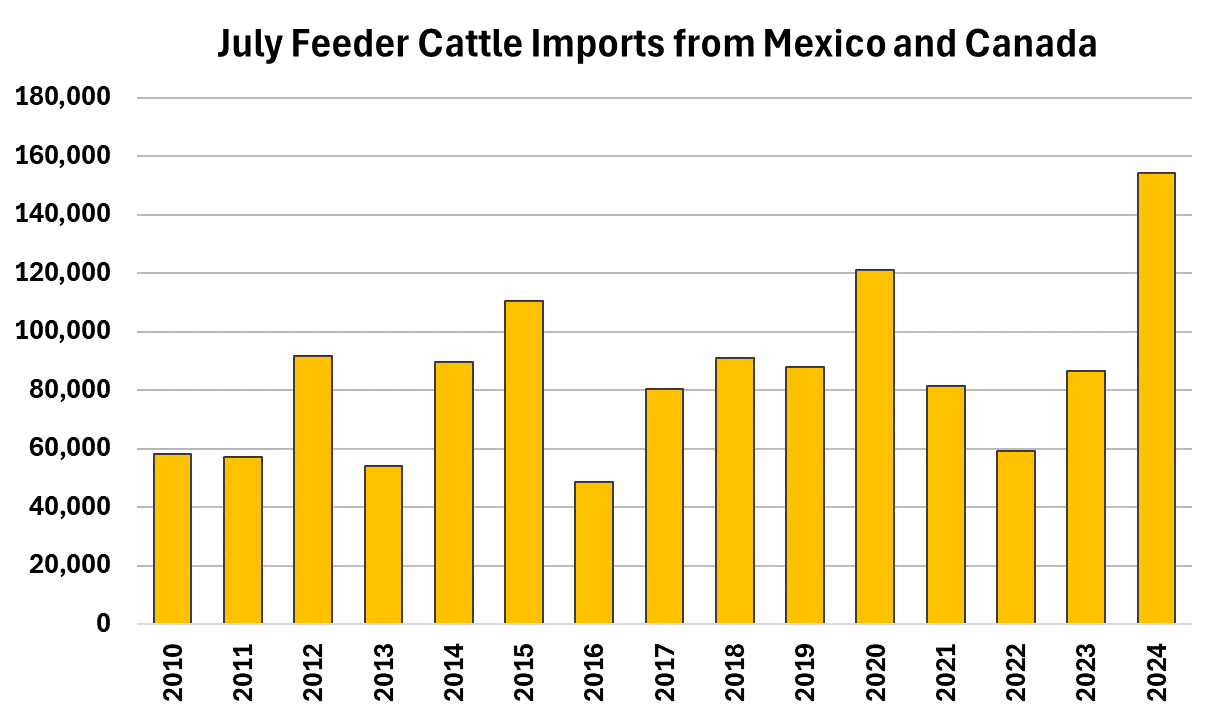

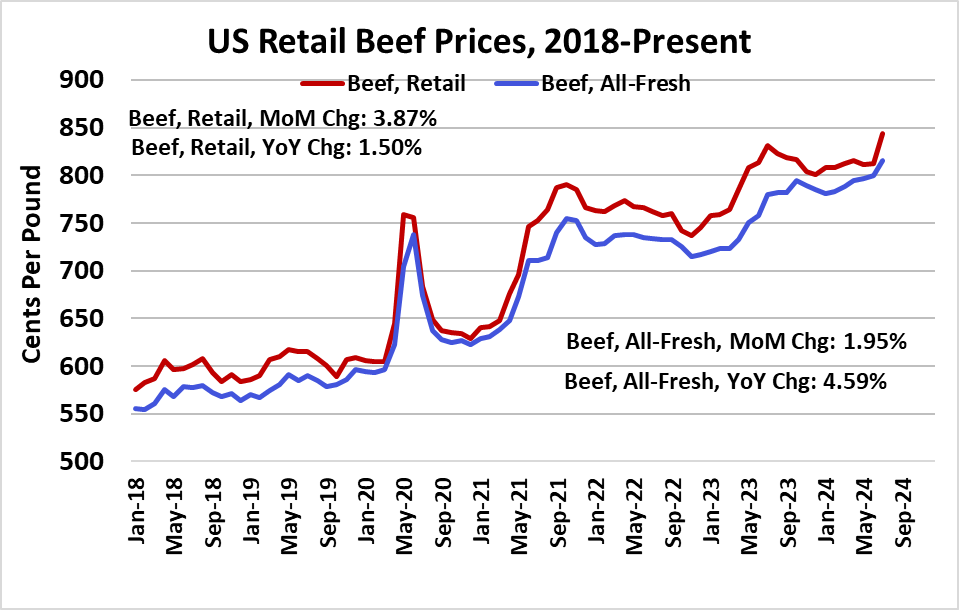

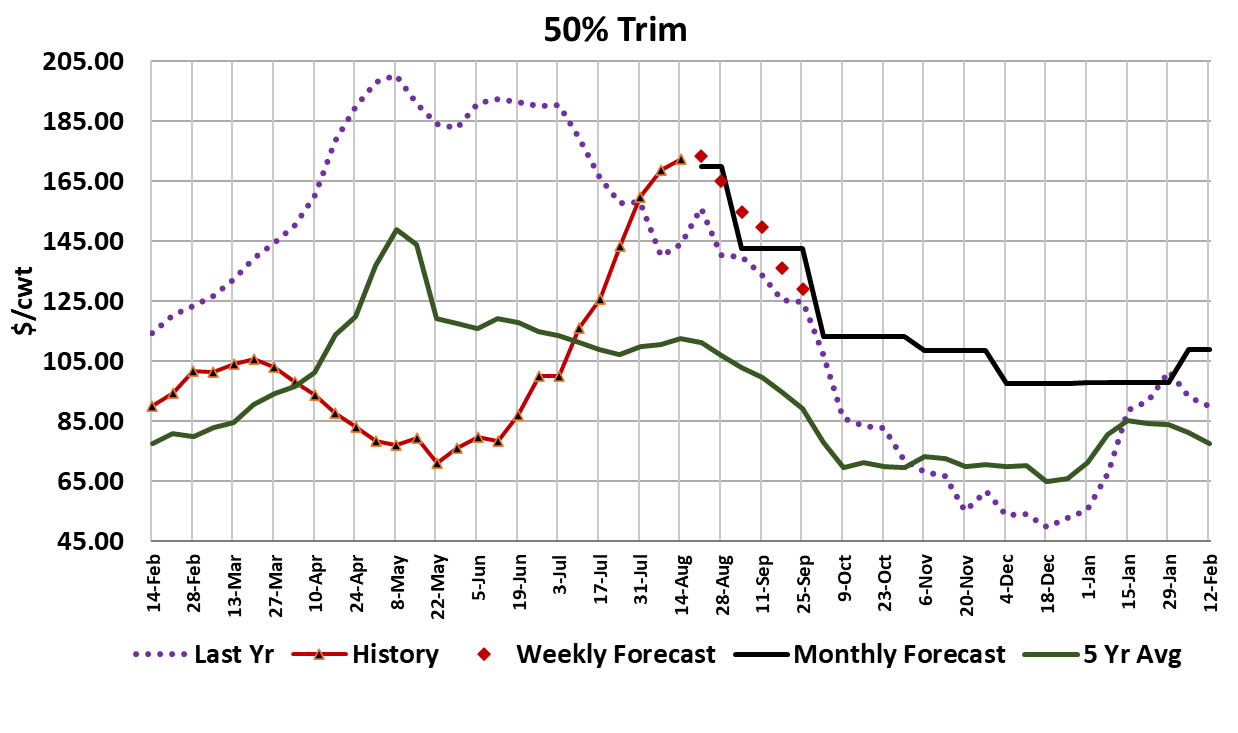

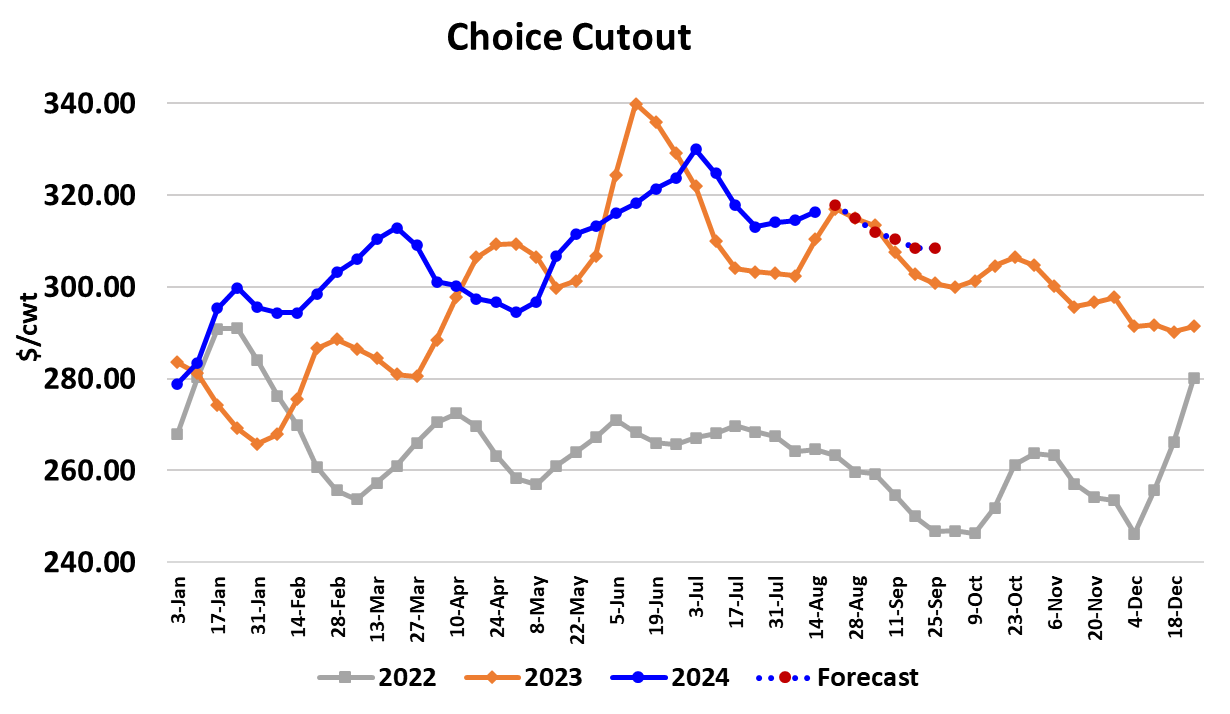

The beef market continued to firm this week with the Choice cutout adding $1.92 on a weekly average basis and the Select cutout up $2.15. The cattle market went the other direction, with trade in the South down $1 at $185 and the live trade in the North down $3 to $190. Packer margins improved as a result, now near -$88/head, which is about $80/head better than just two weeks ago. The futures market threw a hissy fit on Friday as the lower cattle trade developed and erased the gains that had been posted earlier in the week. Traders may have been spooked by the $3 drop in the live price up North, but a narrowing of the North/South spread is pretty common at this time of year and so shouldn’t have been too surprising. Nearby Aug settled just below $183 on Friday, which is $2 under this week’s cash trade in the South. Expiring futures always price to the region where the cheapest cattle are located, which is currently the Southern Plains. With two weeks until expiration, traders are signaling that they expect the cash market in the South to decline another $2 or so between now and the end of the month. That doesn’t seem unreasonable, but it probably also means that there is little additional downside in the Aug contract from here. Once Aug stops retreating, there is a good chance that the rest of the curve will also calm down. Earlier in the week, traders were starting to show some interest in buying the back of the futures curve, which has been beaten down mercilessly in recent weeks, but Friday’s sell-off my have them re-thinking that idea. An inverted futures curve is highly unusual at this point in the cattle cycle where numbers are still shrinking and herd rebuilding has yet to start. What could justify Aug25 $10 below Aug24 when the herd is shrinking? It could be that traders are concerned about a significant softening in demand over the next year that would more than offset the positive price impact of smaller cattle numbers. Beef demand has been very elevated since the pandemic, so there is plenty of room for it to move lower and thus revert back towards the long-run mean. However, every time that I’ve tried to dial back demand significantly in my forecasts over the past few years, I’ve come to regret it because demand has stubbornly refused to comply. Another possibility is that perhaps traders don’t expect cattle and beef supplies to contract much next year. It is hard to look at the domestic supply data and come to that conclusion, but it is possible that the US could start importing very large numbers of cattle from Canada and Mexico to alleviate the shortfall. On the beef side, where imports are already running strong, there is the possibility of bringing in even more beef from abroad next year. Still, it seems like a long-shot to assume that imports will be sufficient to make up for shrinking domestic cattle supplies. A third possibility is that traders expect margin pressure to eventually force packers to close one or more large plants. That would be negative to cattle prices, but supportive to beef prices. A fourth possibility is that traders are just wrong. It wouldn’t be the first time that has happened. It will be interesting to see how this plays out, but for now I’m expecting cattle prices to finally breach the $200 mark sometime next spring or summer. That almost happened this summer when the 5-area price averaged just over $197 in early July. The gains in the cutouts this week were driven largely by the rib primal and probably indicates some last-minute buying ahead of Labor Day. Fat trim pricing remains very elevated, with 50s averaging over $170 this week. The 90s market also remained firm, averaging close to $375. The forecast has the cutouts starting to ease near the end of August and then continuing to soften through September. I don’t think the declines will be huge, maybe $2-3 a week in September, but that would renew the pressure on packer margins because I don’t think that packers will be able to reduce cattle prices enough to offset those losses. Retail prices for July were released this week and it was a shock to see the traditional retail price series gain almost 4% from the previous month. The “all-fresh” price was up close to 2% month-on-month. It does make one wonder how much more beef price inflation the consumer will tolerate. This week’s fed kill clocked in at 488k, up 8k from the week before. I’d expect next week’s kill to be similar or slightly larger. The FI steer carcass weights were reported 2 pounds higher this week and 22 pounds over last year. It is looking like weights are now starting to track higher after being in a mostly sideways pattern since March. Another potential landmine comes next Friday, when USDA will release fresh Cattle on Feed data. My guess is that placements during July could be reported 10% or more above last year and if that comes to pass, it will probably cause another round of hand wringing in the futures market. Ten percent sounds scary for sure, but that is mostly because last year in July placements were exceptionally light. One of the things that makes me think placements will be large is that we saw very strong feeder cattle imports during July. Next week, look for modest gains in the cutout early in the week that could begin to fade near the end of the week as the Labor Day business gets finalized. Cash cattle are probably no better than steady in the South, with some further price erosion likely in the North.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}