Beef Wrap July 26

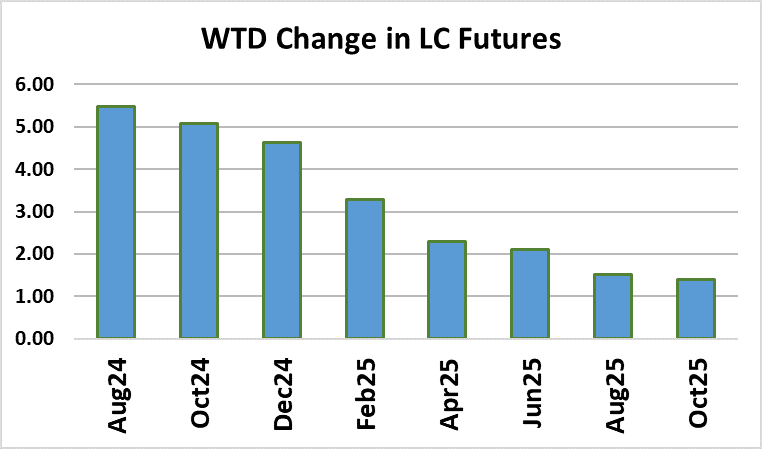

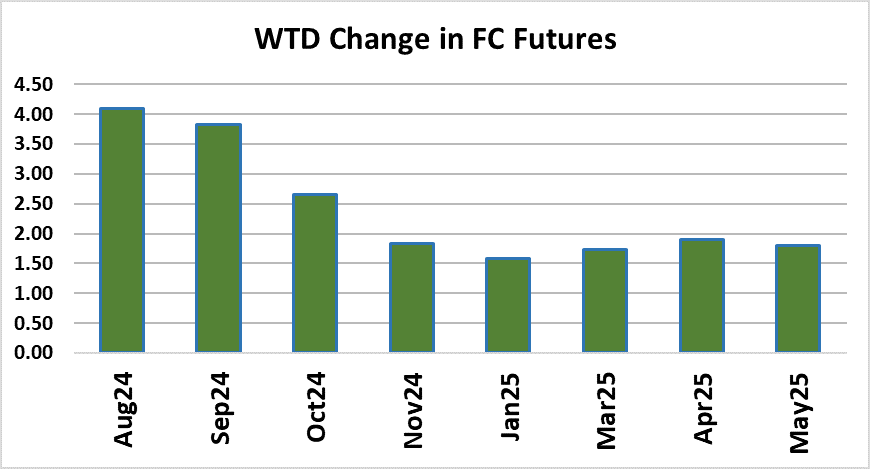

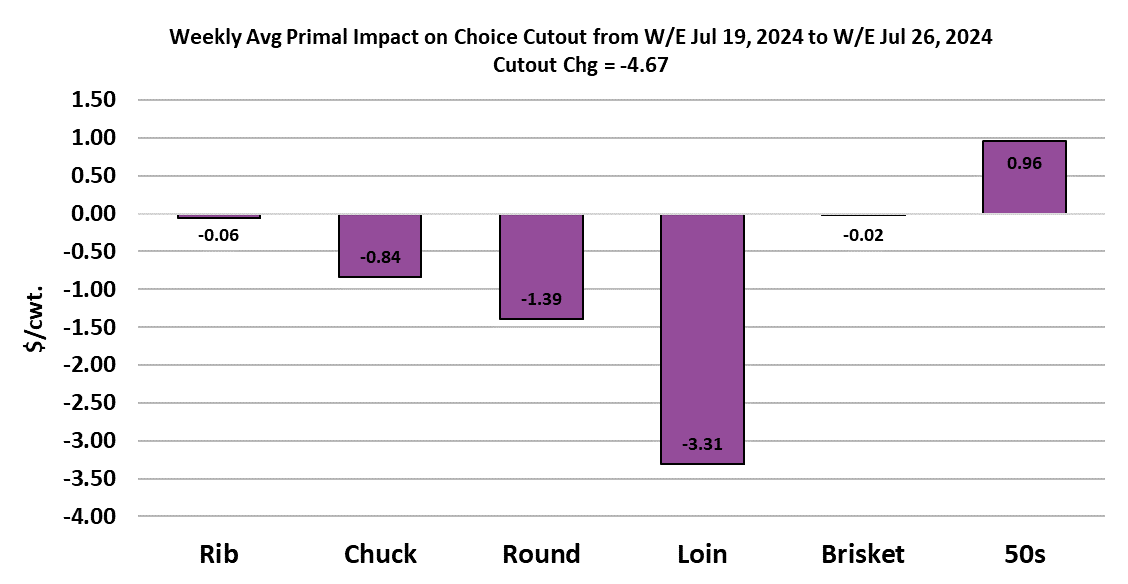

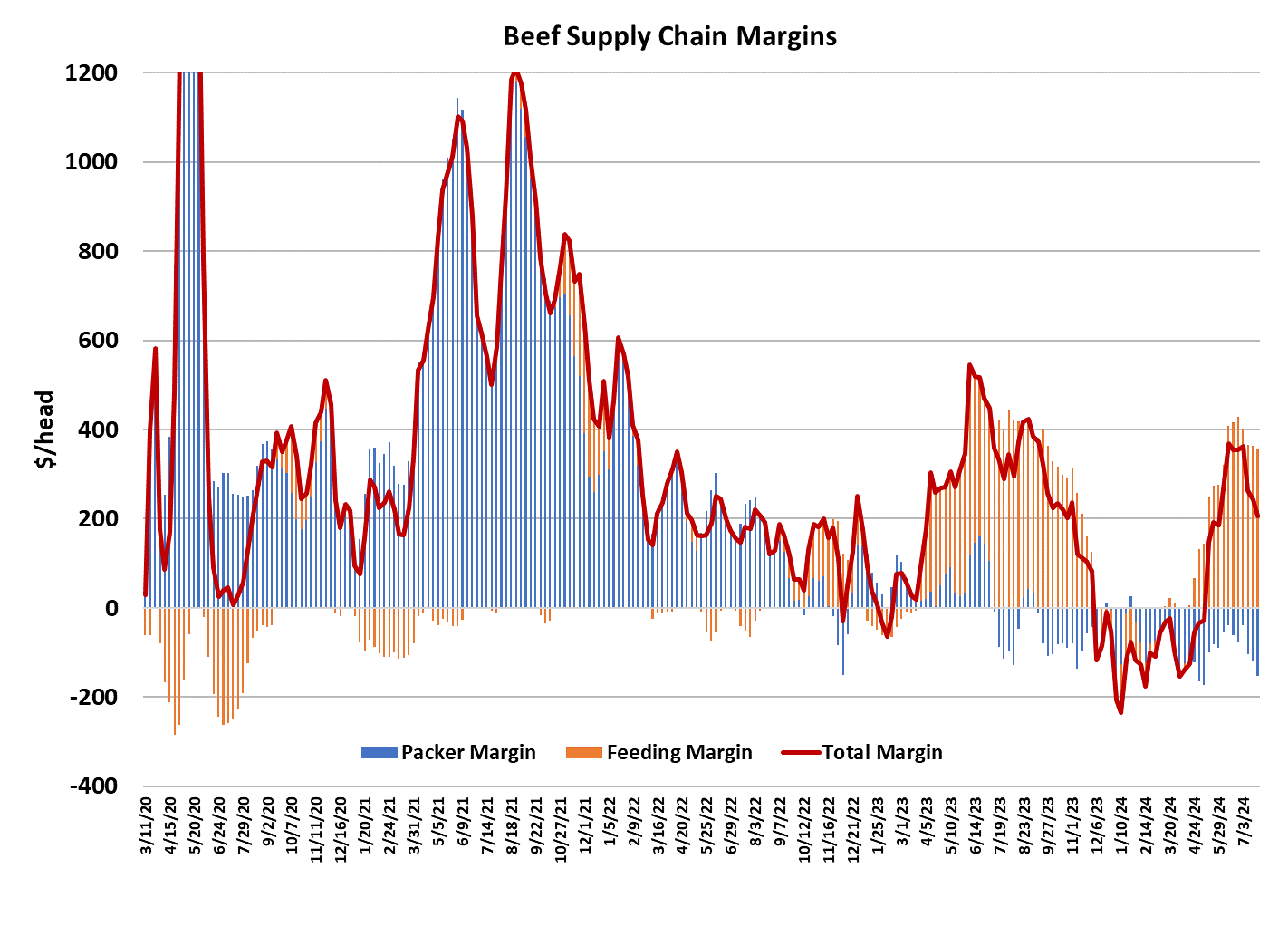

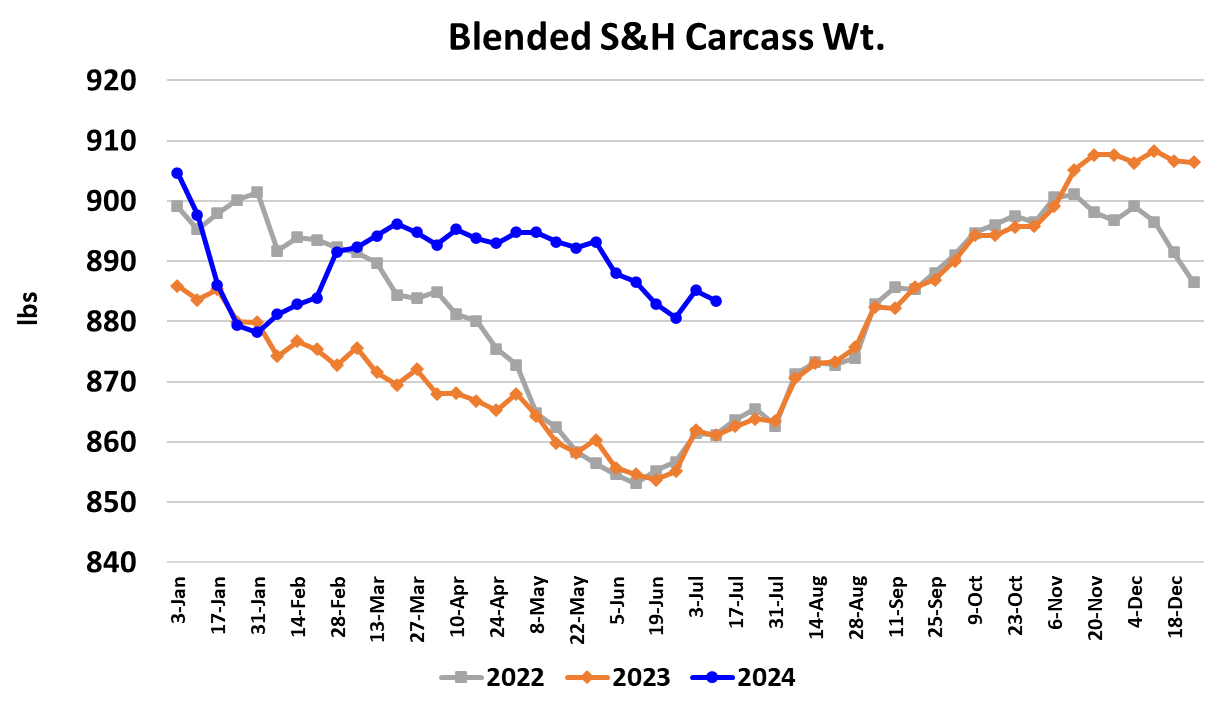

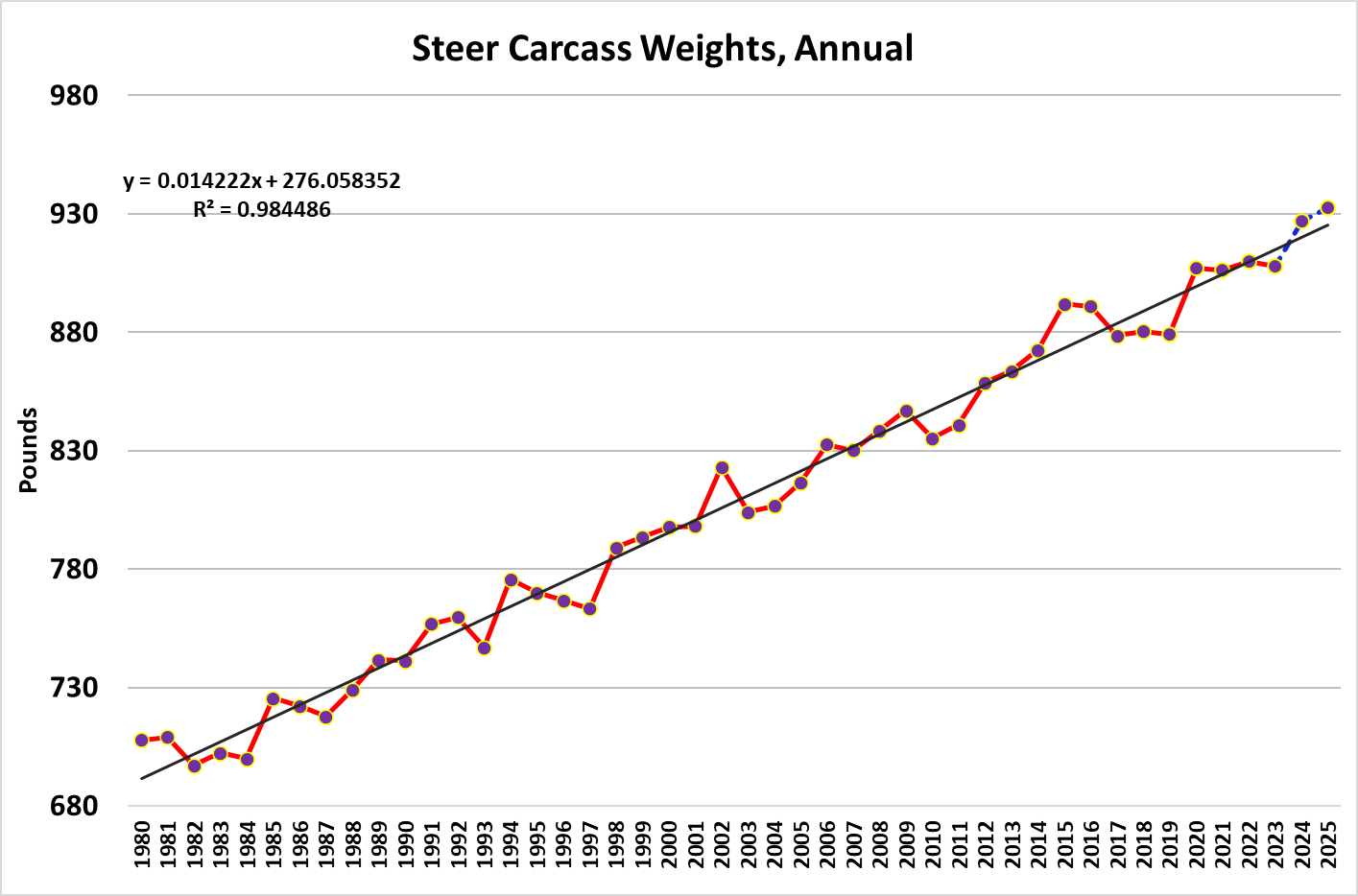

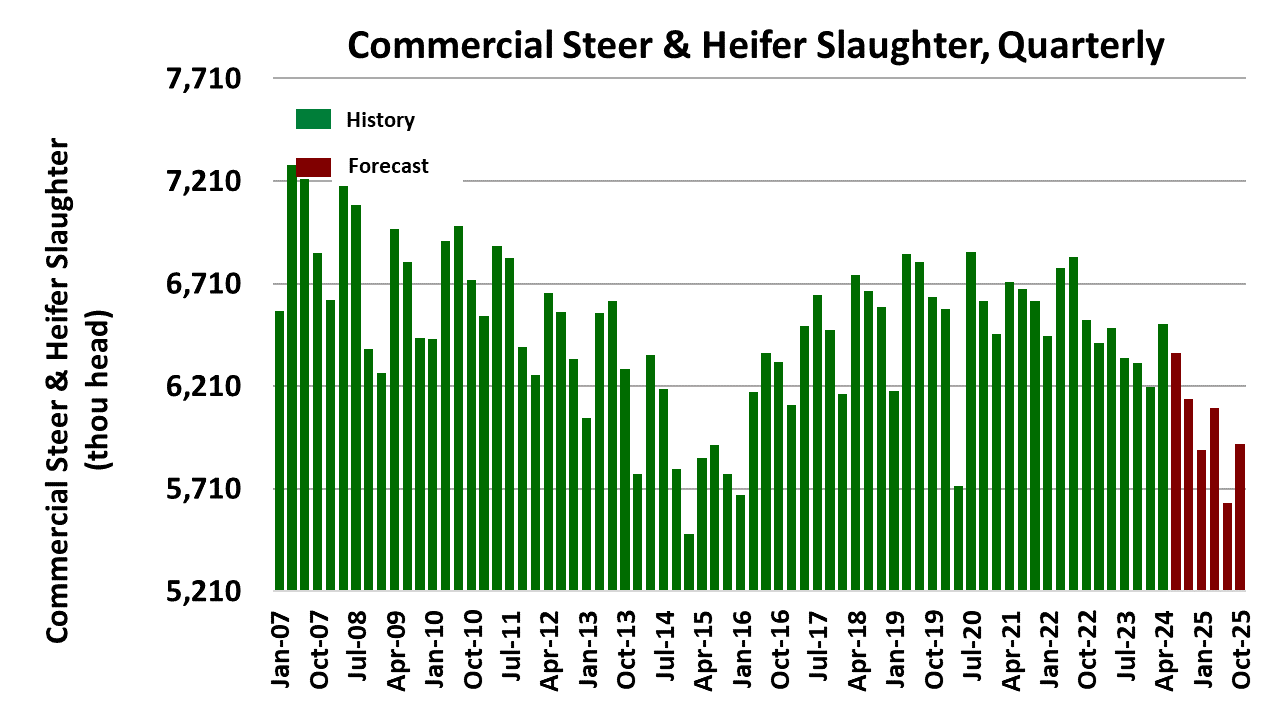

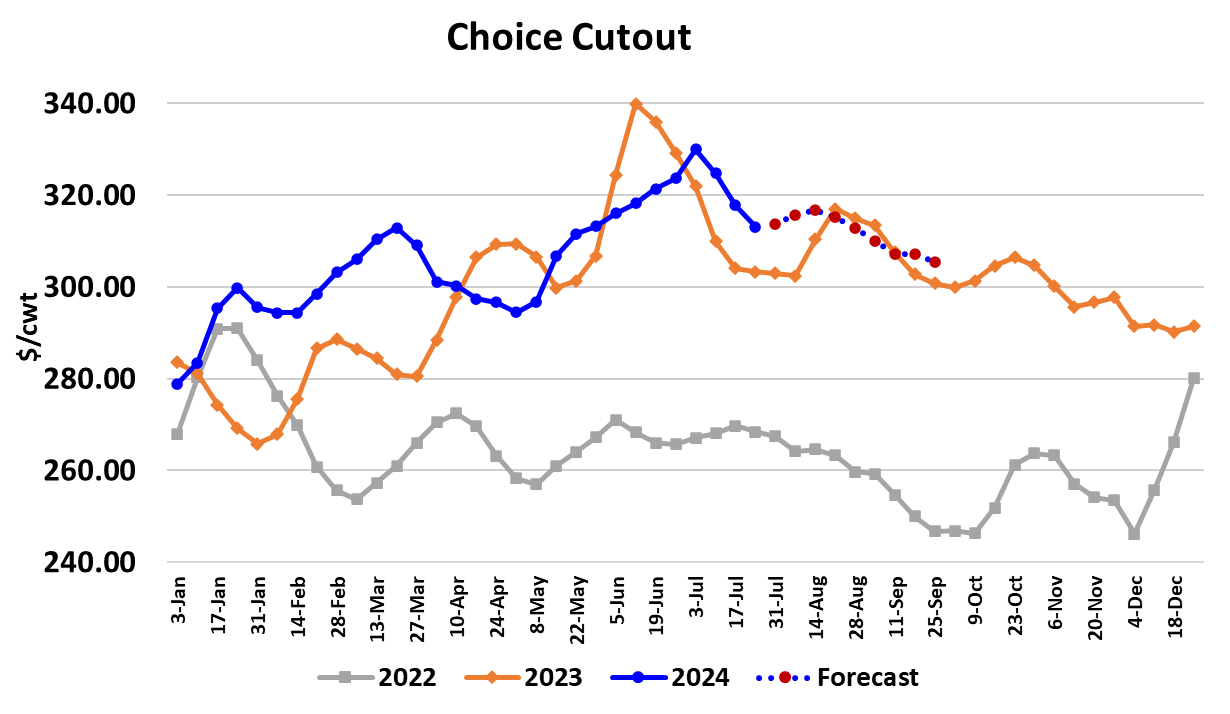

The previous week’s light kill didn’t seem to influence the cutouts much this week as the Choice dropped $4.67/cwt. on a weekly average basis and the Select was down $4.32/cwt. That’s bad news for packers, particularly since cattle feeders managed to reverse the direction of cash cattle prices this week, with prices in all regions moving solidly higher. In the South, cash trade was at mostly $190, up $2 from the week before and in the North trade was established in the $197-198 range, up $1-2 from the prior week. Beef prices down, cattle prices up is not good for packer margins and this week’s margin is estimated to be $153/head in the red. Next week, margins may move even deeper into negative territory because of this week’s gain in cash cattle. Through July, packer margins are averaging about -$90/head and my forecasts for the remainder of 2024 suggest margins in the last five months of the year could be even worse, averaging about -$130/head. It has been over a year since packers last had a monthly average margin that was positive. What is a packer to do? The obvious remedy is to close one or more of the large plants. That would bring capacity into better alignment with the cyclically shrinking supply. At this stage, every packer wants a plant to close but they don’t want it to be one of theirs. In fact, capacity is anticipated to increase over the next year or two as some new, smaller plants come on line. That will just make the cattle supply/packing capacity imbalance worse. So I’m afraid the poor packer margin story is going to be with us for a long time to come. When packers slashed the fed kill two weeks ago, their aim was to pressure cattle prices. Instead, what they ended up with this week was higher cattle prices so they seemed to abandon that strategy by increasing the fed kill to around 490k this week. That is still a little below the 500k that the flow model suggests should be market ready each week. Cattle feeders seem to know that they are in the driver’s seat once again and appear determined to make the most of it. There is a heat wave scheduled to descend on the midsection of the country next week and it could carry on well into August. That won’t be good for cattle weight gains or grading and may give cattle feeders another excuse to hang on to cattle for a little while longer. Unless, of course, packers are willing to pony up more dollars. This week, steer weights were reported one pound lower and heifer weights were three pounds lower. The blended S&H carcass weight is now only 21 pounds heavier than last year, down from 35 pounds just a few weeks back. The upcoming hot weather is likely to cause the YOY gap to narrow even further. There has been a lot of talk in the last few months about heavy carcass weights, but if we zoom out and look at the long run trend in weights we can see (chart attached) that weights were a little under the trendline in 2023 and in 2024 they are moving to a spot just above the trendline. Given that corn prices are way down from last year and animal numbers are shrinking cyclically, it shouldn’t be a surprise that weights are move back over trend. Look at what happened to weights in 2014-2015, the last time cattle numbers were cyclically low and it becomes obvious that 2024 weights are not unusually heavy, but 2025 and 2026 weights could move much higher above the long-run trend. Add to all of this the consumer’s newfound love affair with Prime and high Choice beef and it is easy to understand why cattle feeders are feeding to heavier endpoints. The de-trended and de-seasonalized carcass weights have now moved back below the zero line, so I can feel confident in saying that there is no backlog built up in feedyards. Of course, this week’s cash cattle price increase tells the same story. Even though the Choice cutout has come down about $15 over the past three weeks, I think that overall beef demand remains good. We saw the normal seasonal move lower in middle meats after Independence Day, but that seems to have now run its course. Up next is Labor Day buying, which should help to limit the downside risk in the middles from here. Loins could continue to ease a bit, but ribs may be on the verge of turning higher. End cut prices have declined much less than prices for the middles and they too look poised to stabilize or possibly move higher. Ground beef demand is red hot, with 50s averaging $143 this week and 90s a little over $376. The fundamental forecast has the Choice cutout holding in the $310-320 range through Labor Day. An interesting tug-o-war is likely to materialize in Sep/Oct as the weather cools and retailers shift to more end cut features. They will need to battle with the grinders for that supply and it could cause the end primals to firm up considerably. Users needing ends this fall might be wise to get some booked here in midsummer while prices are a bit soft. This is the time of year when we typically get the mid-year cattle inventory estimates from USDA, but budget considerations caused them to drop that report this year. It is pretty clear that animal numbers are still declining and this year’s calf crop will be smaller than in 2023. I’m currently looking for 2024 calf crop to be down 1.5-2.0%. There’s still very little evidence of herd rebuilding, so cattle and beef supplies may continue to decline for at least a couple more years, maybe longer. Next week, look for the cutouts to stabilize and perhaps post modest gains. Cash cattle should do no worse than steady, with reasonable odds of another price increase.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}