Beef Wrap July 5

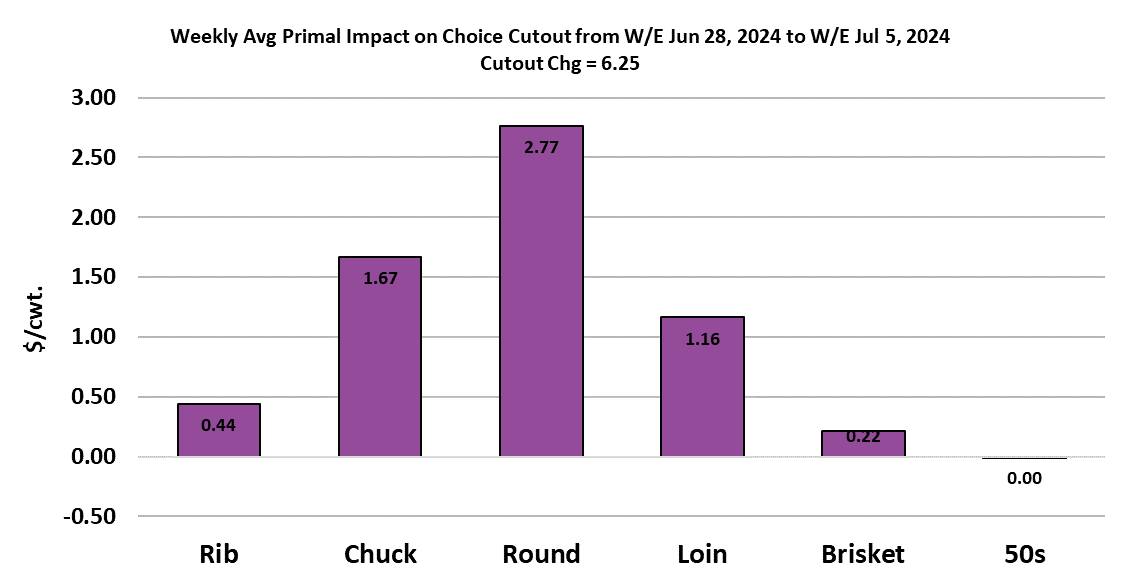

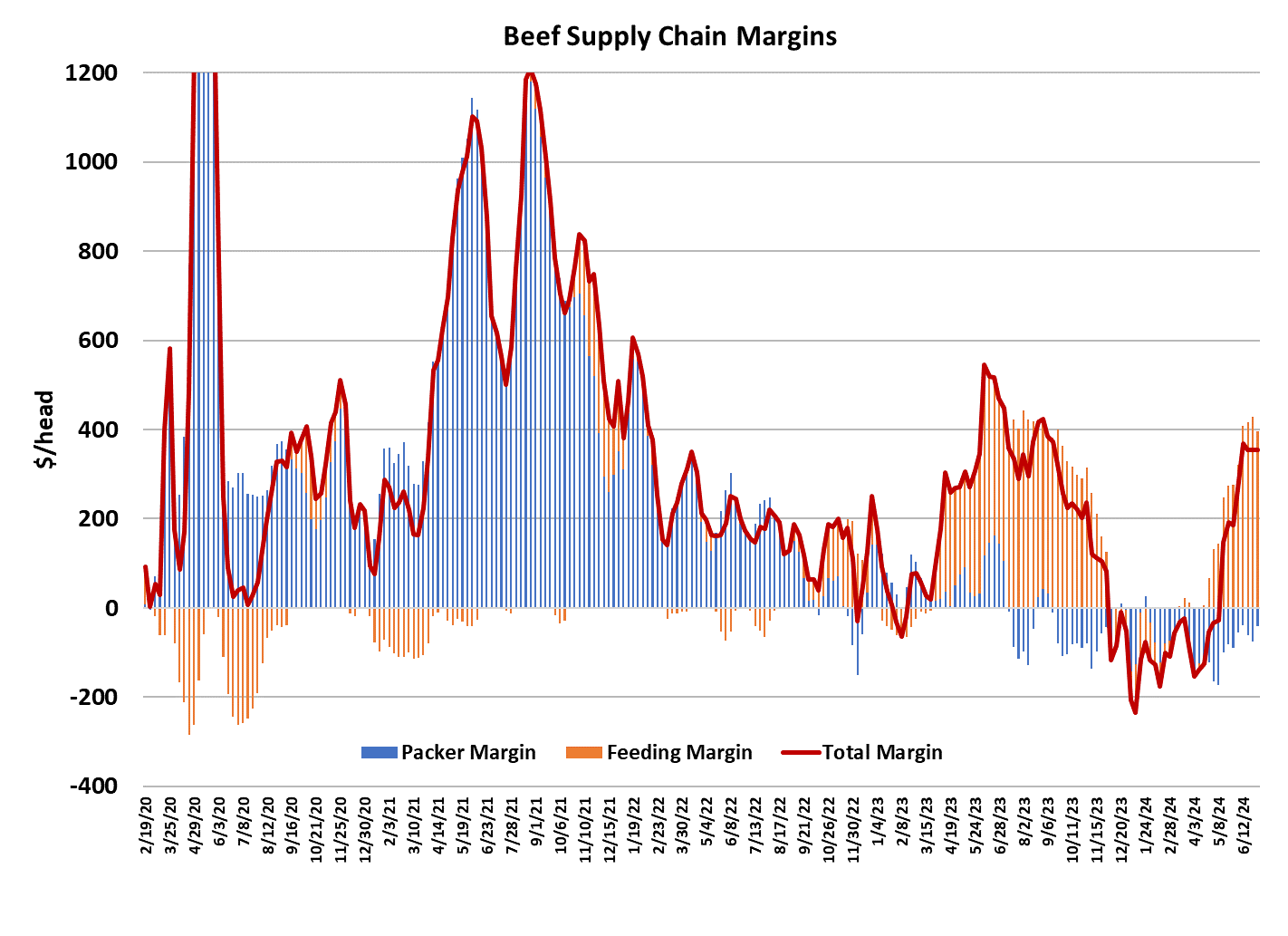

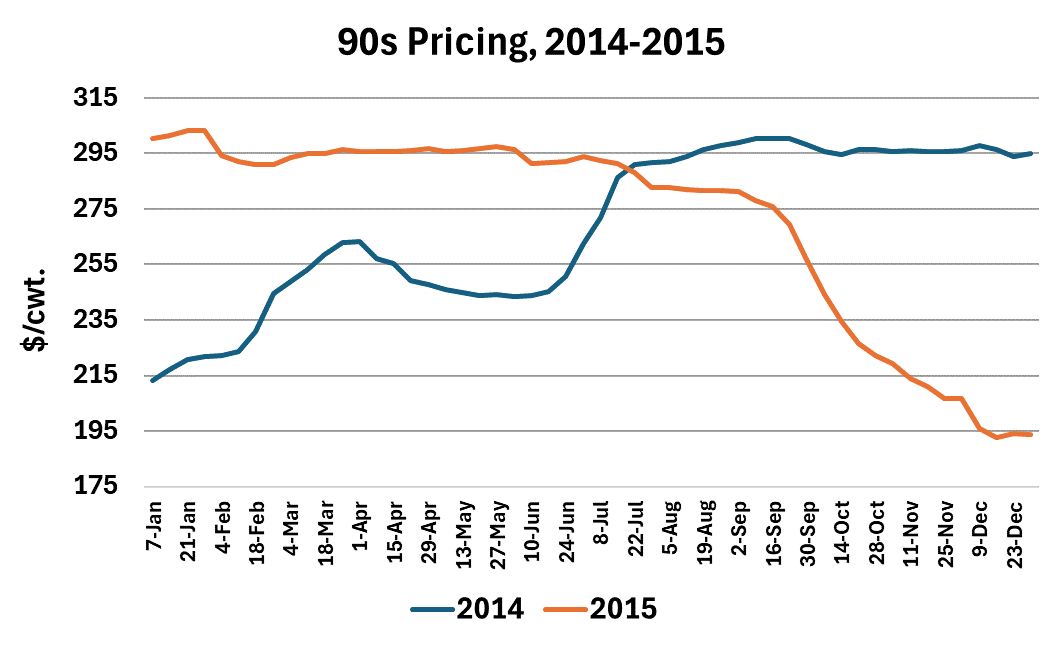

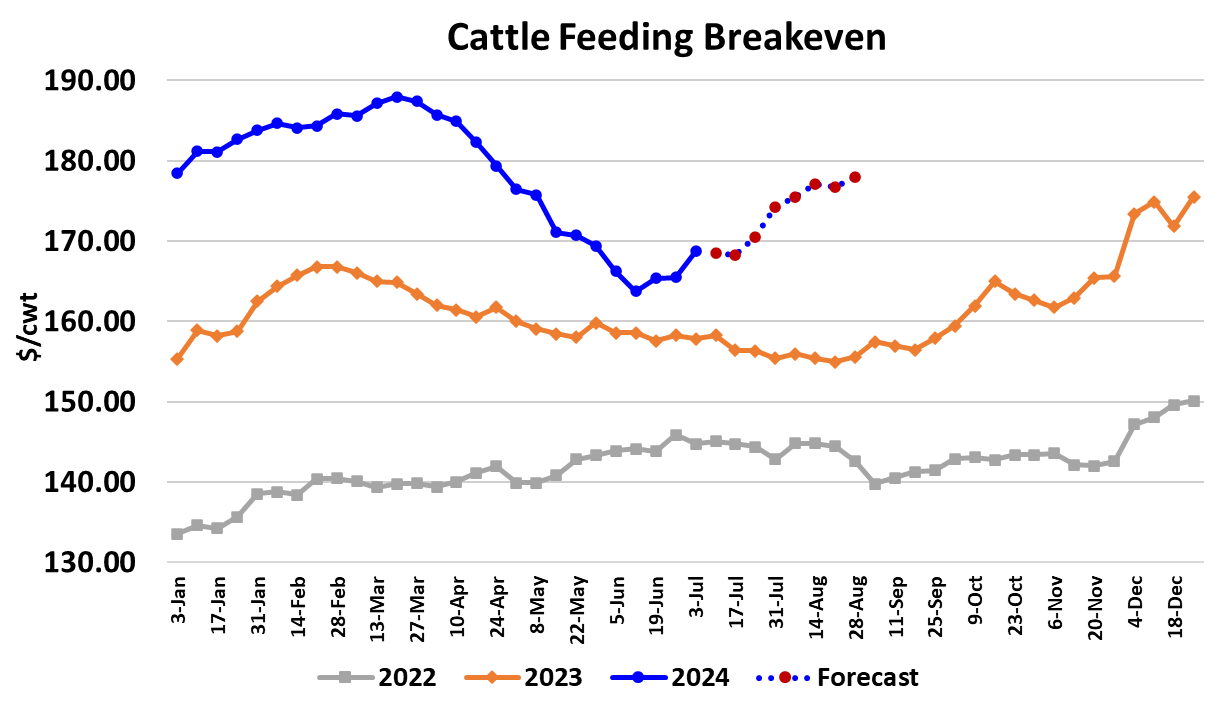

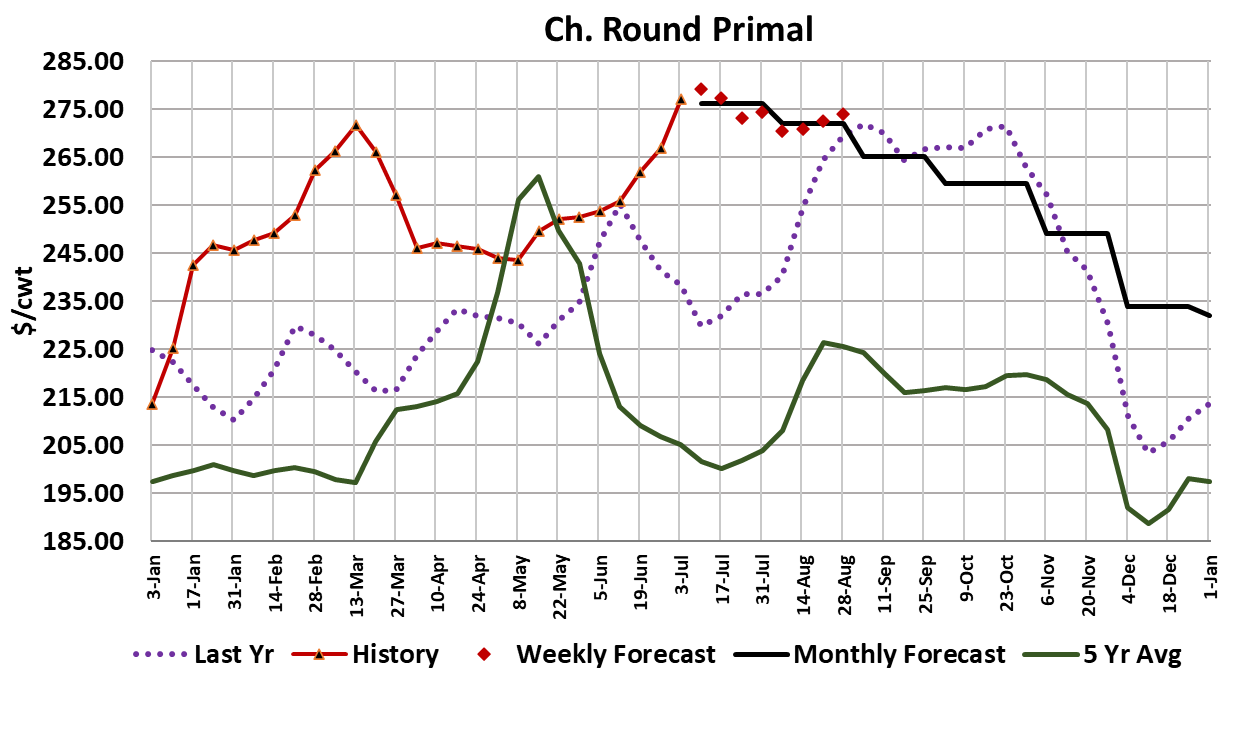

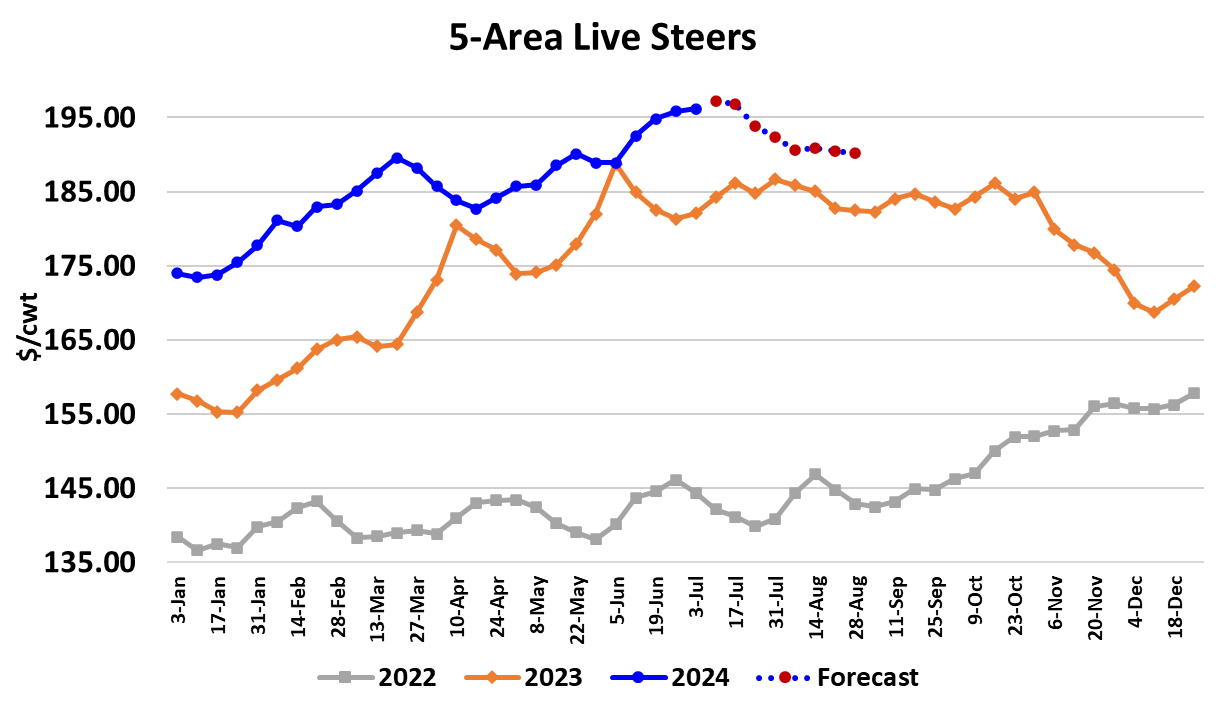

Nobody told beef buyers that the dog days of summer are upon us because they were busy paying up for beef like it was early spring. The Choice cutout added $6.25/cwt. this week on its way to averaging $329.96 and the Select cutout was up $1.60 on a weekly average basis as it moved to $305.58. The attached chart indicates that the big drivers of the gains this week were the round, chuck and loin primals which, incidentally, are the three largest contributors to the cutout. In the past couple of weeks, steer and heifer beef production has been running nearly even with last year yet the round primal was priced 13% stronger than last year and the chuck primal was 4% stronger. That implies much stronger demand for end meats this summer compared to last and the reason is super-high lean beef prices. 90s averaged a little over $372/cwt. this week, which was 27% above the same period last year. It is becoming more and more apparent that the lean beef market is the most important factor in determining the direction of the cutout. If it continues to rise, then the cutout will likely remain firm. Typically, the 90s market tops in June, but last year it didn’t make its top until mid-September. Shortly thereafter, if you recall, the futures market sold off hard and the cash cattle market went into a decline that lasted until early December. The moral of the story is that things look a lot darker for pricing in the cattle and beef complex when 90s prices are falling rather than rising. So it would seem that traders should be intently focused on trying to figure out when the 90s are going to finally start to sink lower. I’ve been thinking that July would mark the top, but the run could extend longer as last year demonstrates. Back in the 2014-15 timeframe, when animal numbers were contracting cyclically as they are now, the 90s kept rising until mid-September 2014 and when they did start to ease, they didn’t go down very much. It was a full year later, in September of 2015, before a material break in the 90s was noted. The attached chart indicates that from mid-2014 to mid-2015 the 90s held firm around the $295 level. If that seems like a long time, consider that the 2014-15 cycle was one where animal numbers made a rather quick bottom and then a quick rise higher. This cycle appears to be taking a lot longer to bottom and turn higher, so it is entirely possible that the strength in 90s prices will also last a lot longer this time around than it did in the last cycle. If that happened, it would probably also mean “higher for longer” on the cutouts and cattle pricing. Just some food for thought. The cash cattle trade this week was a little hard to decipher due to the holiday on Thursday, but it looks like trade in both the North and South will be close to steady with the week before, or perhaps a little higher. So far, it doesn’t look like packers have managed to buy many cattle, so it will be interesting to see what the weekly tally is when USDA releases the complied data on Monday. The combined margin as been mostly steady for the past three weeks, but really looks like it is in the process of making a top. I calculate this week’s packer margin near -$40/head and the cattle feeding margin at +$388/head. My guess is that when the combined margin does start to decline, it will be mostly from feedlot margins declining, while packer margins are likely to stay $50-100/head in the red. Cattle feeding breakevens are now on the rise and should be close to $178/cwt. when Labor Day arrives. The increasing breakeven is largely a result of an escalation in feeder cattle prices that took place near the beginning of the year. Feeder prices have been mostly trending higher since December, so it is a good bet that feedyard breakevens in the second half of this year will continue to work higher. Rising breakevens tend to make cattle feeders tougher negotiators in the cash market, so while we may see some decline in cattle prices over the next couple of months, they aren’t likely to go down in big chunks. This week’s fed kill was estimated at 419k due to the holiday, but next week I’d look for the kill to be back up near the 500k mark. For the balance of July and through August, market-ready cattle supplies should be large enough to fuel fed kills in the 495-505k range. Steer weights were reported 4 pounds lower at 913 pounds in this week’s data, so now we have weights coming down when they should be going up—just the opposite of what happened this spring. Demand is registering as very strong and I’m sure that the lean beef market has a lot to do with that. Going forward, it is typical to see demand ease during the dog days of summer, but that might not generalize well this year. Next week, look for the cutouts to be down a little from this week’s hot level as production returns to normal. I’m reluctant to call cash cattle lower just yet unless the futures correct sharply lower, so steady seems like the safest call there.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}