Pork Wrap June 28

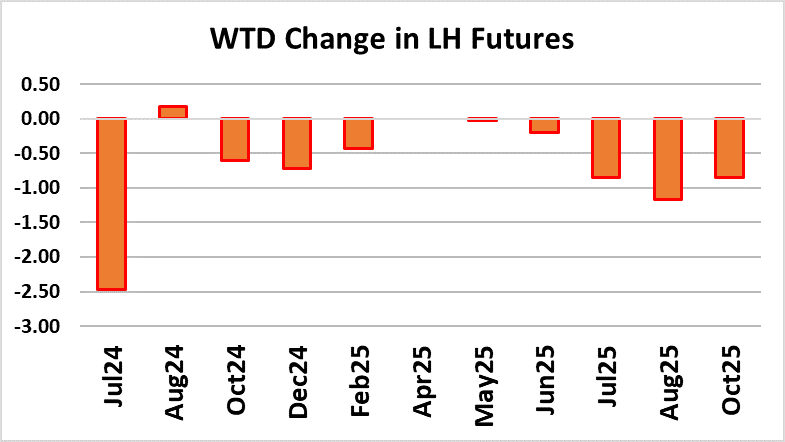

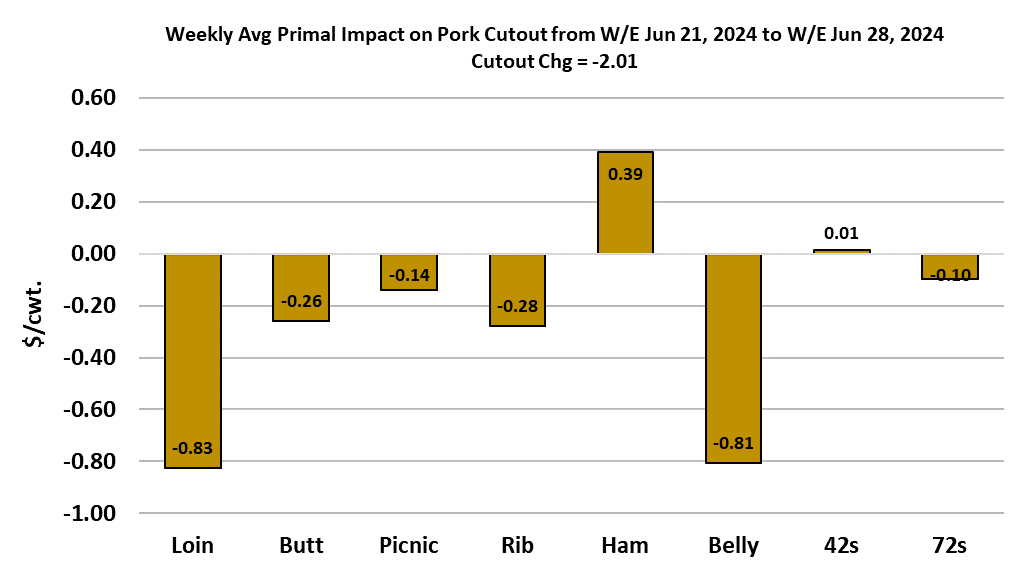

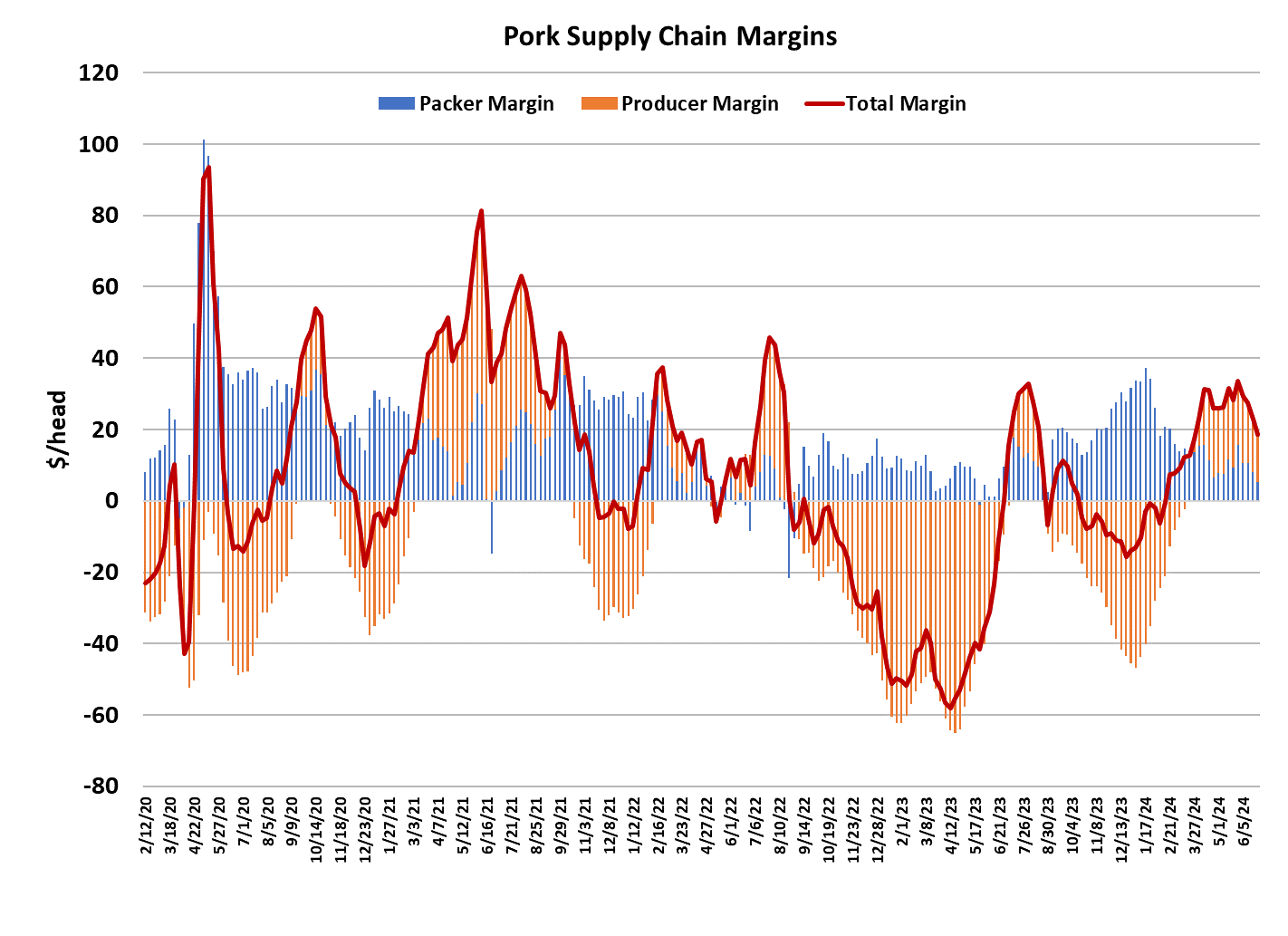

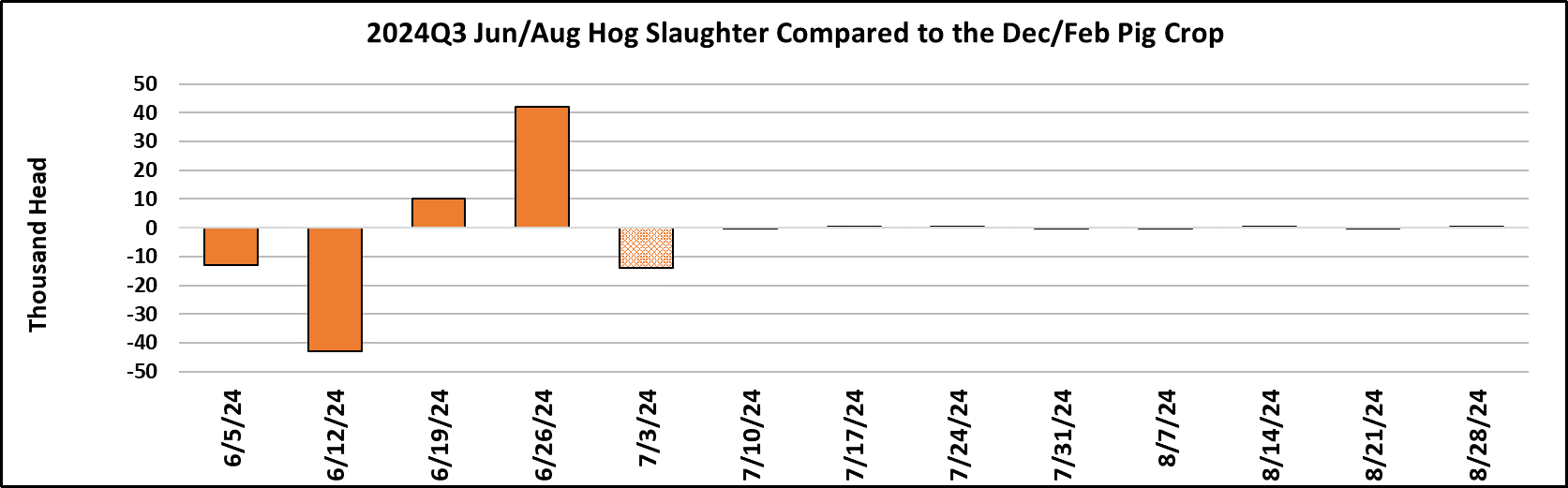

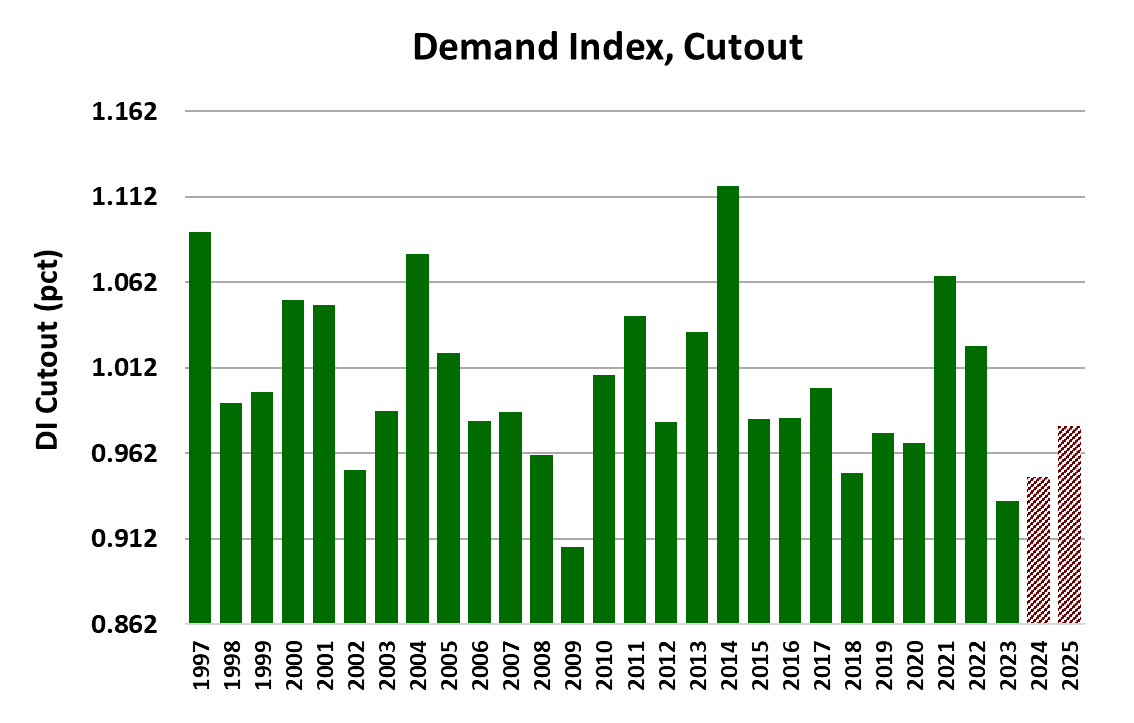

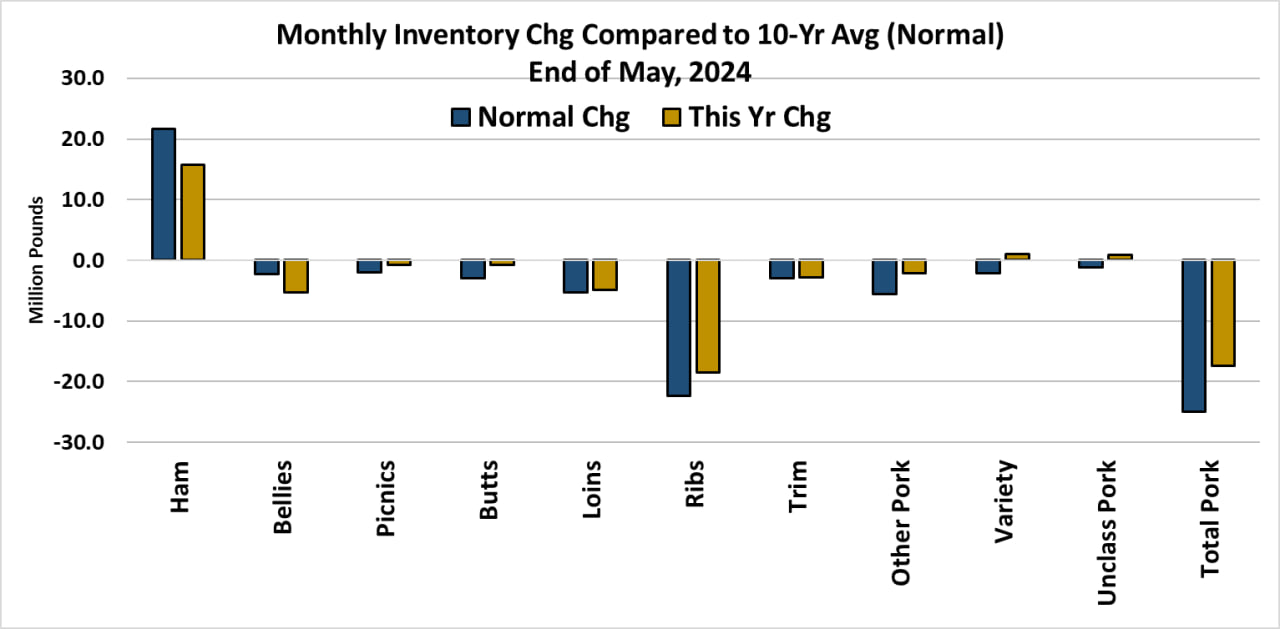

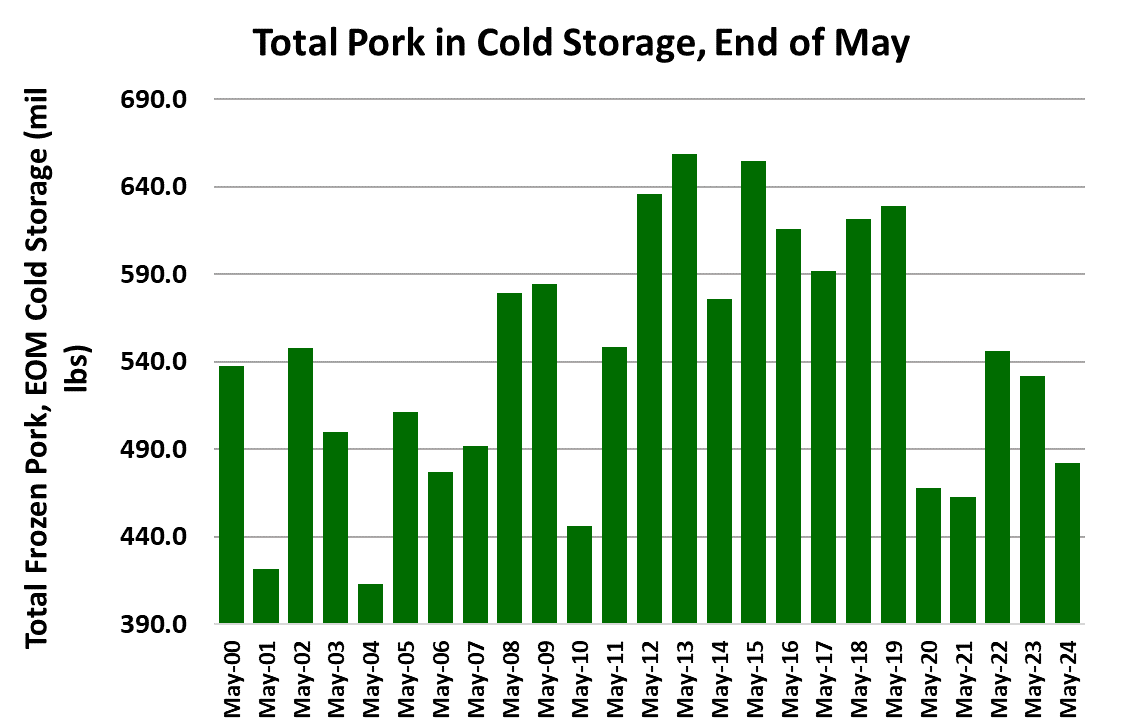

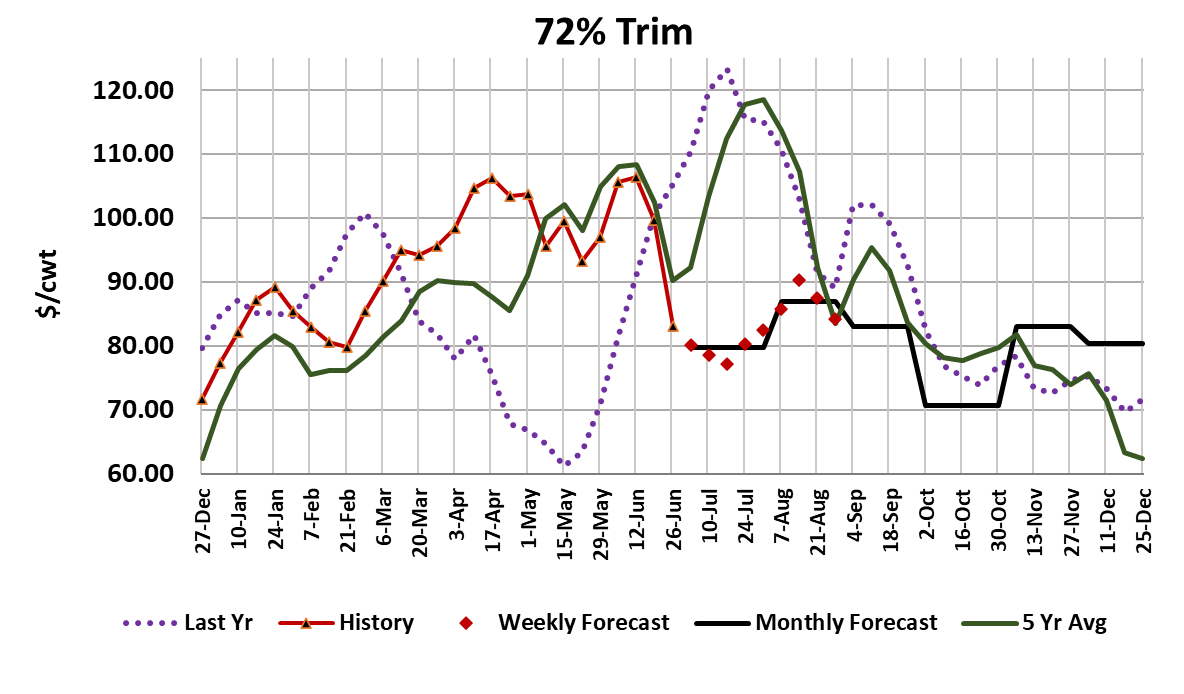

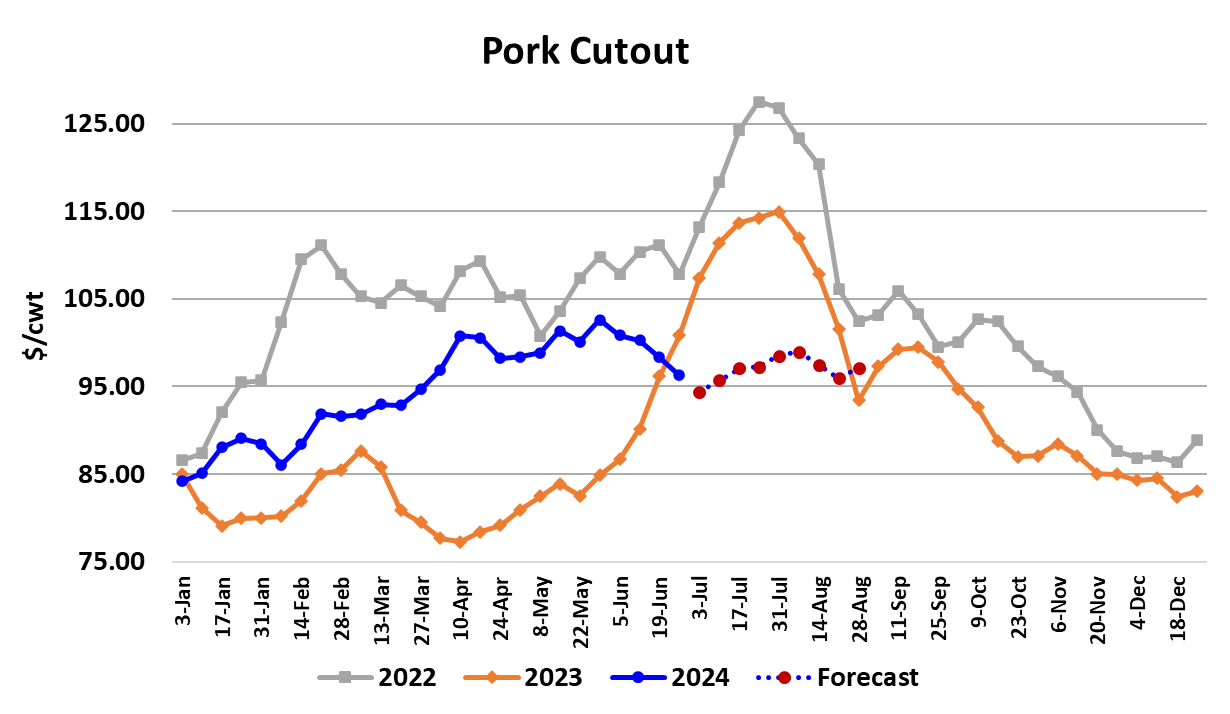

Packer margins came under pressure this week as the cutout dropped and cash hog prices were a little higher. On a weekly average basis, the cutout was down $2.01 to $96.29 while the NDD negotiated market was $1.06 higher to $88.54. That left packer margins at only $5/head—a three-dollar drop from the week before. Of course, this is the point in the calendar when the smallest packer margins normally occur, so this decline isn’t all that surprising. I still think that packers will be able to get through the summer without posting a negative margin. Hog supplies appear relatively ample and we are just 2-3 weeks away from when supplies should start expanding seasonally. Next week’s kill will be shorted by the July 4 holiday, so packers will need fewer negotiated hogs and it may be more difficult for producers to push hog prices upward. Over the past couple of weeks, the cutout has lost $4, going from $100 to $96, and in my opinion this week’s cutout was worse than it printed on paper. It was supported by low volumes, particularly in the ham complex. I don’t like the way the trim market is behaving, with the 72s losing over $15 in the last week and a half and 42s down $10 over that same period. The attached chart shows that pretty much everything except hams were lower on the week and the hams look a little suspect. I’m concerned that packers may be behind on ham sales and could need to move bigger volumes next week, which could limit the ham primal’s ability to support the cutout. We normally see the seasonal top in ham prices around the end of July, so there could be some further increases to come, but my confidence in that isn’t all that strong at this point. Bellies seem to be going nowhere fast, actually easing over the past couple of weeks. Interestingly, the belly primal is now almost dead on where it was last year at this time, and last year from the end of June to the end of July the belly primal added a whopping $110/cwt. I don’t think we are going to see a repeat of that this year, but it does highlight the fact that we are in that part of the calendar when the belly market can go crazy. The combined margin is clearly trending lower, suggesting that we’ve entered another short-term downcycle in demand. The last upcycle was unusually long, running from January through May and that makes me wonder if this new downcycle might also be a lengthy one. Some observers have postulated that pork prices are suffering because Prop 12 is seriously crimping consumption in California, leaving more product that must clear the market in the other 49 states. That is entirely possible, but it seems odd to me that this would suddenly show up now given that Prop 12 has been enforced since the beginning of the year. However, we did see a big jump in the May retail pork prices and that might be a symptom of high retail pork prices in California spilling over into the national average. If Prop 12 and similar laws in other states are going to lift retail prices and thus curb consumption, the industry needs to get serious about reducing the pork supply. This week’s Hog & Pigs report made it clear that producers aren’t thinking in that direction yet. They did reduce the breeding herd a tiny bit from it’s March 1 level, but strong productivity more than negated that effort and as a result the March/May pig crop was up 1.8% YOY. Those are hogs that will be slaughtered in the upcoming Sep/Nov quarter, so it is pretty clear that we are going to have more hogs this fall compared to last. Given that slaughter capacity was reduced a bit this year with the closing of some smaller plants, getting all of those hogs dead this fall could be a challenge. Packers will find a way to make it happen, but they will need to be incentivized with strong margins and that likely means weak hog pricing this fall and the potential for deep losses by producers. Maybe that is what it will take to bring about the needed production cuts. Producers have seen sharp reductions in the cost of feed over the past year, so naturally that has made them want to increase production, but they have yet to see the revenue consequences of doing so. That could come later this year. That said, if demand could just return to “normal” levels, pricing would be much better and the losses for producers would be smaller. Overall pork demand has been unusually weak for the past year and a half, so I’m hopeful that 2025 will be the year when demand reverts to the mean. This week’s Cold Storage report showed a smaller-than-normal drawdown of pork stocks during May, but the difference probably isn’t large enough to affect near-term pricing. Total pork in cold storage is still 9.4% smaller than last year. This week’s slaughter totaled 2.42 million head, almost even with the prior week. The holiday should trim next week’s slaughter to about 2.1 million head. After that, the forecast has weekly slaughter holding around 2.4 million head for three weeks before it starts to grow in August. Next week, look for some further easing in the cutout unless the hams or bellies post a surprise increase. Cash hogs should be steady to slightly weaker.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}