Pork Wrap August 25

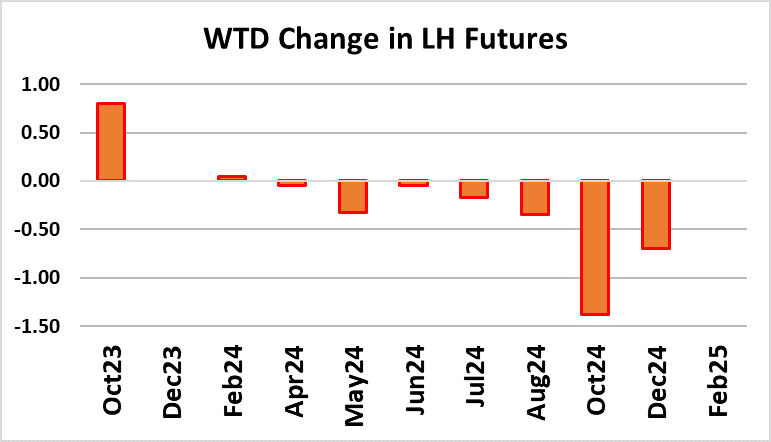

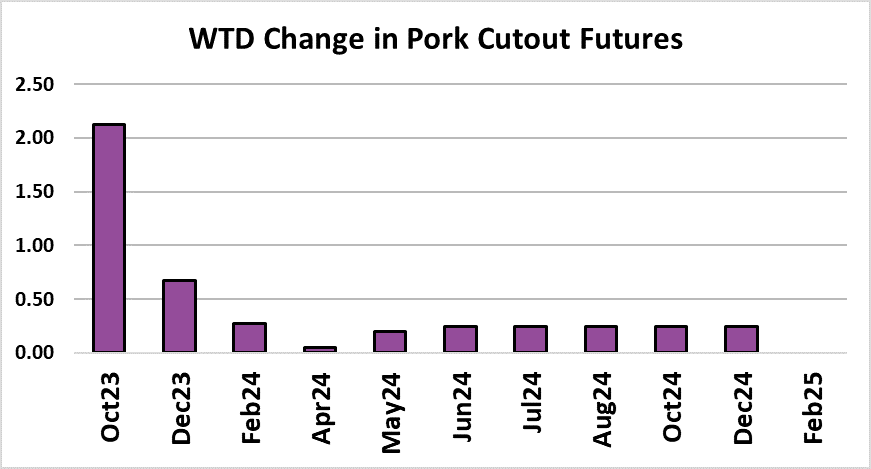

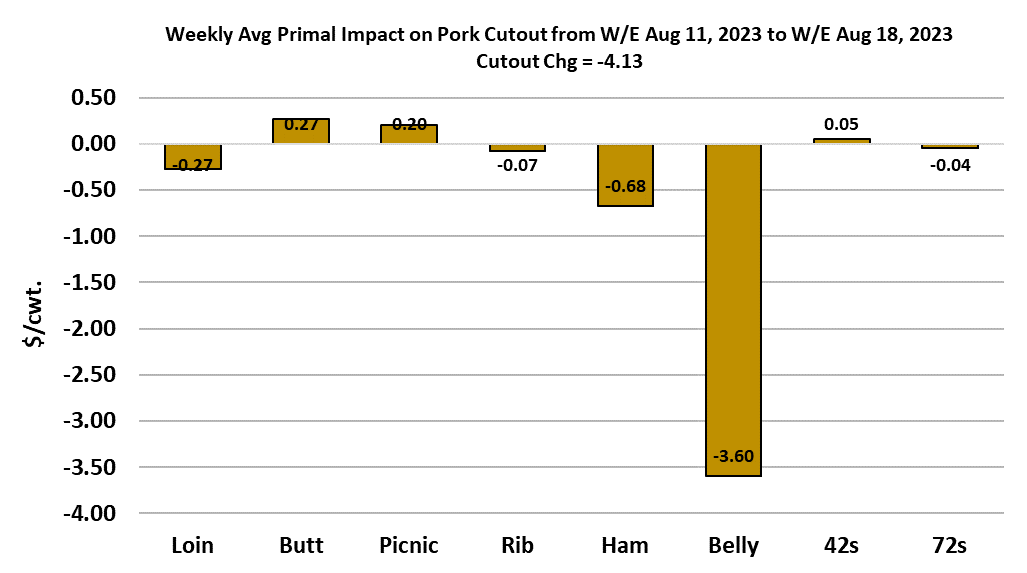

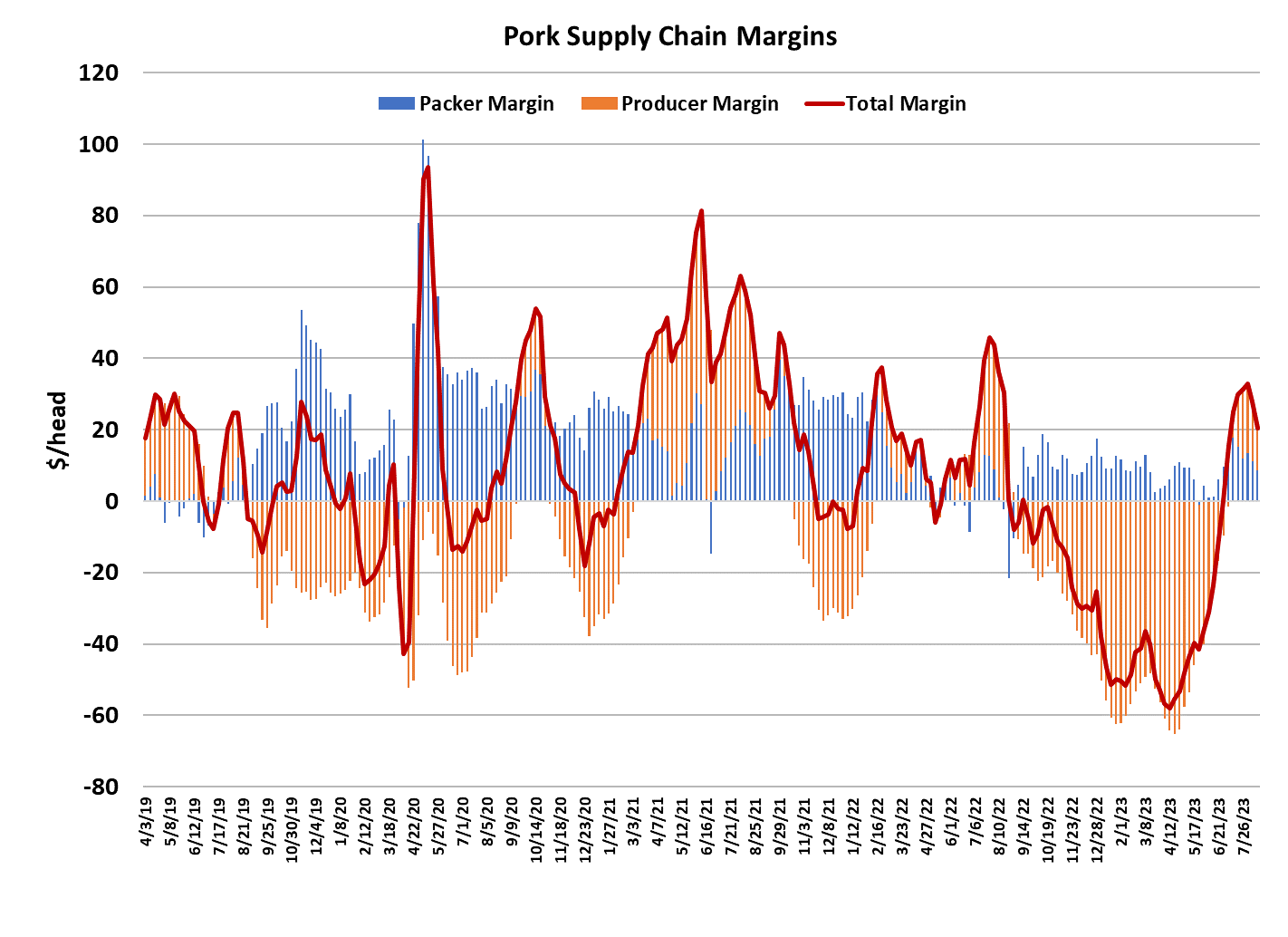

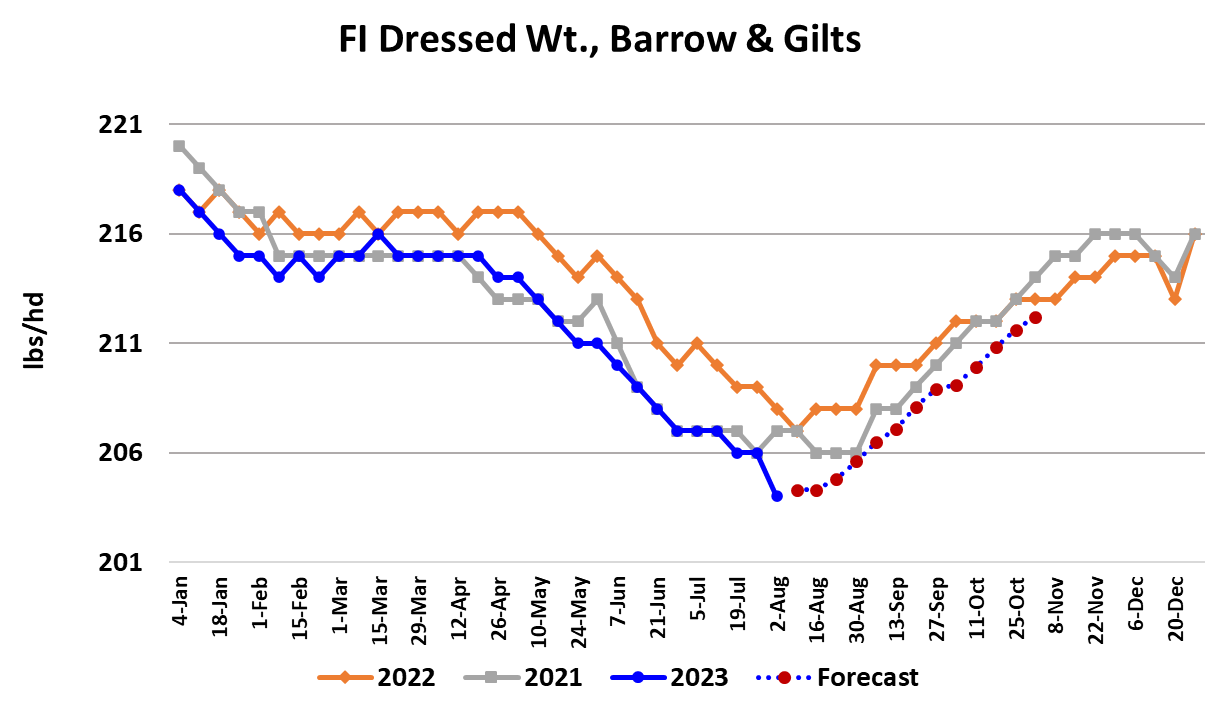

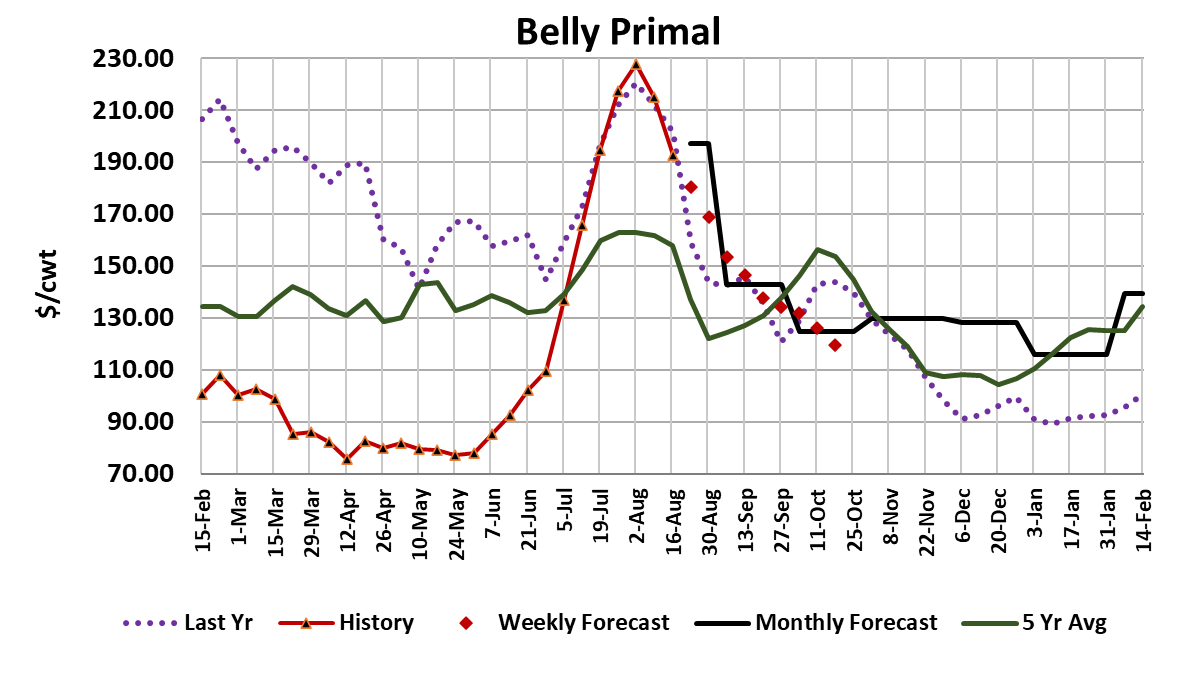

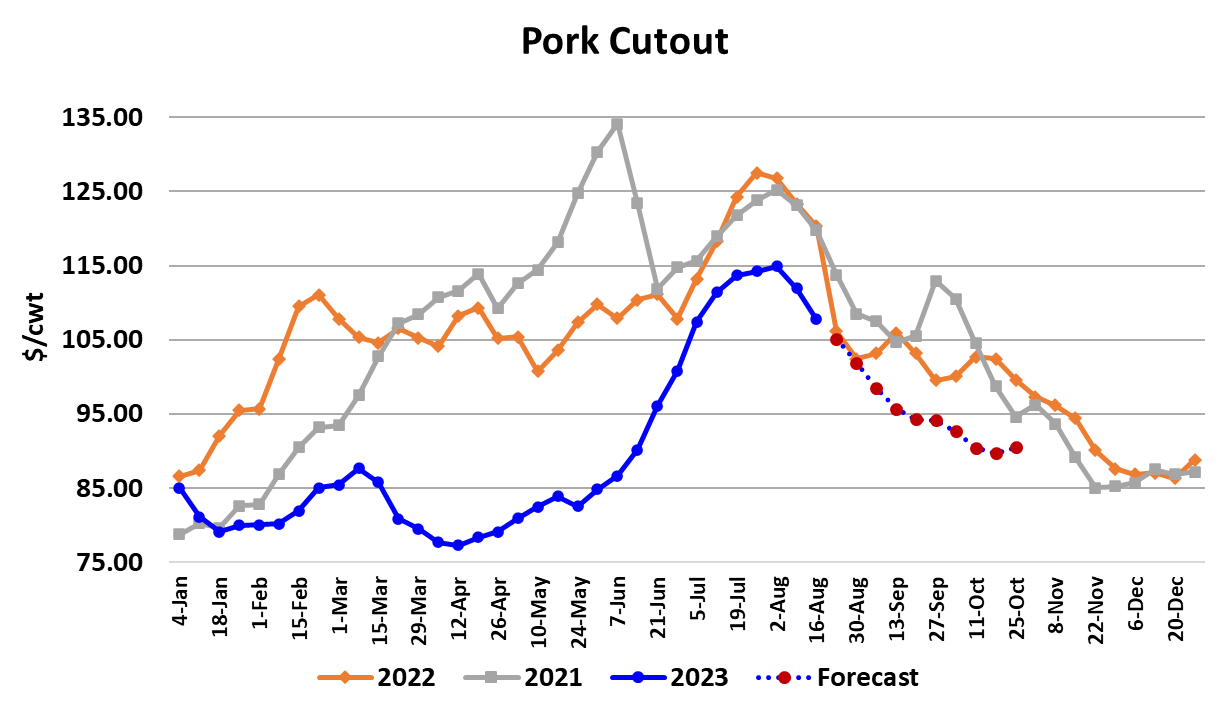

Well, it finally happened. Bellies came crashing down today, with the primal falling an eye-popping $58/cwt. in a single day. That, in turn, drove the cutout $11 lower on the day. Interestingly, nearly the exact same thing happened to bellies on August 23rd last year. That marked the beginning of a very long bear market that lasted until April of this year. Is history about to repeat itself? I think that the market is in a strong downcycle that will probably last through most of September, but I don’t expect that to carry into the spring of next year. In fact, sometimes we see a modest demand bump in late Sep or early Oct that could repeat this year. But for now, the focus is on the cutout and how low it might eventually go. Outside of the huge belly price decline today, there are other elements in the pricing picture that don’t look particularly good. Ham prices are softening, negotiated hog prices are moving lower at a fast clip, and the weekly kill finally reached 2.5 million head. For those that are holding out hope that the belly primal will reverse today’s drop, don’t. It is more likely that this was the first step in a bigger downtrend for bellies rather than a hiccup that will get quickly reversed. The rapid decline in the cutout will pinch packer margins intensely, and they will likely respond by pressuring the negotiated hog market intensely next week. Of course, these days a lot of hog pricing formulas reference the cutout, so we should see a very rapid decline in the LHI over the next few days. If the cutout and negotiated hog prices stayed where they are today, then the LHI would likely print below $89 by the end of next week. Factor in further losses in the cutout and the negotiated markets and suddenly we are looking at the possibility of a LHI in the mid $80s by early September. Futures traders have yet to grasp the gravity of the situation as the Oct contract only lost $0.65/cwt. today. I would look for further downward correction early next week. On a weekly average basis, the cutout was down $6.19/cwt., but Friday-to-Friday, the cutout was down $12.75/cwt. The attached chart shows that, in addition to the problems the bellies have caused, the hams are also pressuring the cutout lower. 23/27 bone-in hams were quoted on Friday at $84.32 and just 8 days ago they were above $100. It is a deadly combination when both the hams and bellies are trending in the same direction. And the scary thing about it all is that kills are just now starting to expand seasonally. Packers put in a big Saturday this week that brought the weekly total up to 2.5 million head. That means a lot of pork that needs to be marketed next week. Of course, kills over the next two weeks should be tempered by the Labor Day holiday, but after the holiday week, expect the weekly kill to bounce back to 2.5 million head and then slowly expand toward a 2.6 million head-per-week peak in November. Near-term however, I am concerned about how well the market will handle this week’s big production. It seems like some further price reductions will be necessary in order to keep inventories manageable. Processors often scale back on raw material purchases ahead of a holiday week and that could mean less demand next week for things like bellies, hams and trims. The short kill weeks won’t be kind to negotiated hog prices either and that is another concern. About the only bullish feature in this market is exceptionally low hog weights and the potential for further weight losses due to the heat wave that enveloped the midsection of the country this week. Barrow and gilt weights printed steady at 204 pounds this week and that could be the annual low unless this week’s heat was intense enough to shave a bit more off of weights. In either case, we are right on the cusp on weights starting to move seasonally higher for the balance of the year and so any dip in weights is likely to be short-lived and not a huge market factor. The WCB negotiated market dropped $5.14/cwt. on a weekly average basis and I suspect that it could lose that much or more next week as packers move into margin protection mode. After the big drop in the cutout, packer margins are a little less than $5/head this week. Of course, all of this week’s drop in the cutout and negotiated markets isn’t yet fully reflected in the LHI, so when that process is complete margins should look a little better. After the belly crash last August, the NDD negotiated price dropped $17 in three days. That is how packers manage margins—they just push the negotiated market lower. With hog supplies increasing seasonally and two short kill weeks on the horizon, I suspect that producers’ ability to resist lower pricing will be minimal. Exports continue to run relatively strong and as prices come down this fall, we should see better overseas movement. That won’t be enough to stop the price declines, but it might slow them, particularly as we enter Q4. Suddenly however, their seems to be a lot more items on the bearish side of the ledger in the hog and pork complex than on the bullish side. The conventional wisdom has always been that the hog market turns bearish after Labor Day, but that bearishness seems to have come a week earlier both this year and last.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}